Business math is the study of mathematics required by the field of business. By the fact that you are reading this textbook, you must be interested in a business field such as accounting, marketing, human resources, or economics.

Regardless of your path, you cannot avoid dealing with money and numbers. Both personally and in your career you certainly use elementary arithmetic such as addition, subtraction, multiplication, and division. However, there is a whole field of mathematics that deals specifically with money. You will be offered loans, lines of credit, mortgages, leases, savings bonds, and other financial tools. Do you know what these are and how these financial tools can maximize your earnings and minimize your costs? Do you have what it takes to execute smart monetary decisions both personally and for your business? Do you know how interest works and how it gets calculated? If you can answer “yes” to these questions, then you are already off to a great start. If not, by the end of this textbook you will have a better understanding of all of these topics and more.

How Do I Learn about Business Math?

Let’s be realistic. In some areas of life and business, you can achieve a reasonable degree of understanding just by reading. However, reading about business mathematics without doing it would be disastrous. To succeed, you must follow a structured approach:

Always read the content prior to your professor covering the topic in class.

Attend class, ask questions, and explore the topic to advance your understanding.

Do the homework and assignments—you absolutely must practice, practice, and practice!

Seek help immediately when you need it. Learning mathematics is like constructing a building. Each floor of the building requires the floor below it to be completed first. In mathematics, each section of a textbook requires the concepts and techniques from the sections that preceded it. If you have trouble with a concept, you must fix it NOW before it causes a large ripple effect on your ability to succeed in subsequent topics. So the bottom line is that you absolutely cannot replace this approach—you must follow it.

About this Textbook

This textbook covers topics from Chapters 8 to 13 inclusive adapted from the original Business Math: A Step-by-Step Handbook by J. Olivier and Lyryx Learning Inc. View the original text for free at Business Math: A Step-by-Step Handbook . Reused under a CC BY-NC-SA license.

This resource uses LaTex and a MathJax plugin to render math formulas. Please note that “some screen readers support MathML, MathJax’s internal format. Screen readers like ChromeVox, JAWS (on IE), and TextHelp support MathJax directly (most only version 2); other screen readers are supported by the assistive-mml extension as of version 3.0.1.” (MathJax Consortium, 2021). It is important to also note that the quality of screen reader support varies greatly with the software you are using and the various settings enabled. For more information on MathJax and screen reader support please visit the MathJax Consortium Accessibility Features page.

Original Book Citation

Author: J. Olivier Publisher: Lyryx Learning Inc. Book title: Business Math: A Step-by-Step Handbook Book version: 2021B Publication date: July 19, 2021 Location: Calgary, Alberta, Canada Book URL: https://lyryx.com/subjects/business/business-mathematics/

About the Authors

Sanja Kraishnik, BA, BEd, MMath

Sanja, the lead on this OER project, has taught math in the Business School at Conestoga College ITAL, in Kitchener, Ontario, for ten years. Sanja’s dedication to ensuring that math is accessible to all students is demonstrated by using LaTex and the MathJax plug-in for Pressbooks to render math formulas and her dedication to ensuring this OER met accessibility requirements. To learn more about using Latex and Pressbooks, review Using LaTex in Pressbooks by Sanja Krajisnik and Jelena Loncar.

Jelena Loncar-Vines, OCT, MSc, BEd

Jelena is a faculty member in the School of Business at Conestoga College ITAL and can be reached at jloncarvines@conestogac.on.ca. Jelena has been a mathematics educator for 14 years, 11 of which have been at the post-secondary level. Jelena’s career focus is to help make mathematics relatable and accessible to students. In addition to teaching, Jelena has volunteered on mathematics education-focused organizations, both provincial and local. Jelena is a life-long learner and enjoys active participation in professional development opportunities geared toward mathematics, post-secondary education, and effective use of technology in the classroom. The development of this OER, and the opportunity for close collaborations with colleagues, has been a very rewarding experience.

Carol Leppinen, Honours BMath, BEd, Honours Specialist Mathematics

Carol is a faculty member in the Business School at Conestoga College ITAL, in Kitchener Ontario and can be reached at cleppinen@conestogac.on.ca. Carol has been a full-time professor at Conestoga College ITAL since 1998 where she has taught Business Mathematics, Statistics, and Quantitative Methods. Prior to that, Carol taught Mathematics and Computer Science at the secondary school level for 5 years. Carol has been a career teacher and is passionate about her students. Carol is grateful for all that her students have taught her over the years.

This project is made possible with funding by the Government of Ontario and through eCampusOntario’s support of the Virtual Learning Strategy. To learn more about the Virtual Learning Strategy visit: https://vls.ecampusontario.ca.

Acknowledgements

3

Gratitude and Thanks

We wish to express our gratitude and thanks to the long list of people who supported and participated in this project.

Leadership Team

With thanks and gratitude, to our leadership teams for their support and encouragement in this endeavour.

Conestoga College ITAL:

Barbara Kelly PhD, Vice-President of Academic/Student Affairs/Human Resources and Research

Gary Hallam M.Sc., Vice President, International & Executive Dean School of Business, School of Hospitality & Culinary Art

Michelle Grimes PhD, Dean School of Business

Jeff Fila PhD, Director of Special Projects

Amy Gleiser, BA, MA, Chair School of Business

Support Teams

Holly Ashbourne, Hon. BA, MLIS Conestoga College ITAL, liaison to accessibility and library supports, for providing a final review, and countless support with Pressbooks technology through workshops, diving into Pressbooks to have a look, and answer numerous questions.

James Yochem, Hon. BA, MLIS Copyright Coordinator, Conestoga College ITAL for answering numerous copyright and copy edit questions.

Antonina Gousseva, BA, Dipl. LIT, Conestoga College ITAL for ensuring this resource met all accessibility requirements.

Kimberlee Carter, BEd., MA, Open Educational Resources (OER) projects consultant, Conestoga College ITAL for spearheading this OER project and keeping us on track.

Juliet Conlon, MLS, Conestoga College ITAL for support in searching out existing OER.

Chapter 8

I

Learning Objectives

Demonstrate the concept of simple interest.

Determine the number of days between two calendar days using the pre-programmed financial calculator method.

Calculate the amount of interest, principal, time, interest rate, and maturity value of investments and loans.

Calculate equivalent payments that replace another payment or a series of payments.

Use simple interest in solving problems involving business applications such as savings accounts, short term guaranteed investment certificates (GICs), treasury bills, and commercial paper.

8.1: Simple Interest: Principal, Rate, Time

1

Simple Interest: Principal, Rate, Time

Simple Interest

In a simple interest environment, you calculate interest solely on the amount of money at the beginning of the transaction (amount borrowed or lent).

Assume $1,000 is placed into an account with 12% simple interest for a period of 12 months. For the entire term of this transaction, the amount of money in the account always equals $1,000. During this period, interest accrues at a rate of 12%, but the interest is never placed into the account. When the transaction ends after 12 months, the $120 of interest and the initial $1,000 are then combined to total $1,120.

A loan or investment always involves two parties—one giving and one receiving. No matter which party you are in the transaction, the amount of interest remains unchanged. The only difference lies in whether you are earning or paying the interest.

The Formula

where,

I is Interest Amount. The interest amount is the dollar amount of interest that is paid or received.

P is Present Value or Principal. The present value is the amount borrowed or invested at the beginning of a period.

r is Simple Interest Rate. The interest rate is the rate of interest that is charged or earned during a specified time period. It is expressed as a percent.

t is Time Period. The time period or term is the length of the financial transaction for which interest is charged or earned.

Important Notes

Recall that algebraic equations require all terms to be expressed with a common unit. This principle remains true for Formula 8.1, particularly with regard to the interest rate and the time period. For example, if you have a 3% annual interest rate for nine months, then either

The time needs to be expressed annually as of a year to match the yearly interest rate, or

The interest rate needs to be expressed monthly as per month to match the number of months. It does not matter which you do so long as you express both interest rate and time in the same unit. If one of these two variables is your algebraic unknown, the unit of the known variable determines the unit of the unknown variable. For example, assume that you are solving Formula 8.1 for the time period. If the interest rate used in the formula is annual, then the time period is expressed in number of years.

Example 8.1.1: How Much Interest is Owed?

Julio borrowed $1,100 from Maria five months ago. When he first borrowed the money, they agreed that he would pay Maria 5% simple interest. If Julio pays her back today, how much interest does he owe her?

Solution:

Step 1: Given information:

P = $1,100; r = 5%; per year; t = 5 months

Step 2: The rate is annual, and the time is in months. Convert the time period from months to years;

For Julio to pay back Maria, he must reimburse her for the $1,100 principal borrowed plus an additional $22.92 of simple interest as per their agreement.

Solving for P, r or t

Four variables are involved in the simple interest formula, which means that any three can be known, requiring you to solve for the fourth missing variable. To reduce formula clutter, the triangle technique illustrated in the video below will help you remember how to rearrange the simple interest formula as needed.

For $95,000 to earn $1,187.50 at 5% simple interest, it must be invested for a three-month period.

Exercises

In each of the exercises that follow, try them on your own. Full solutions are available should you get stuck.

If you want to earn $1,000 of simple interest at a rate of 7% in a span of five months, how much money must you invest? (Answer: 34,285.71)

If you placed $2,000 into an investment account earning 3% simple interest, how many months does it take for you to have $2,025 in your account? (Answer:5 months)

A $3,500 investment earned $70 of interest over the course of six months. What annual rate of simple interest did the investment earn? (Answer: 4%)

In the examples of simple interest so far, the time period was given in months. While this is convenient in many situations, financial institutions and organizations calculate interest based on the exact number of days in the transaction, which changes the interest amount. To illustrate this, assume you had money saved for the entire months of July and August, where or of a year. However, if you use the exact number of days, the 31 days in July and 31 days in August total 62 days. In a 365-day year that is or t = 0.169863 of a year. Notice a difference of 0.003196 (0.169863 – 0.16) occurs. Therefore, to be precise in performing simple interest calculations, you must calculate the exact number of days involved in the transaction.

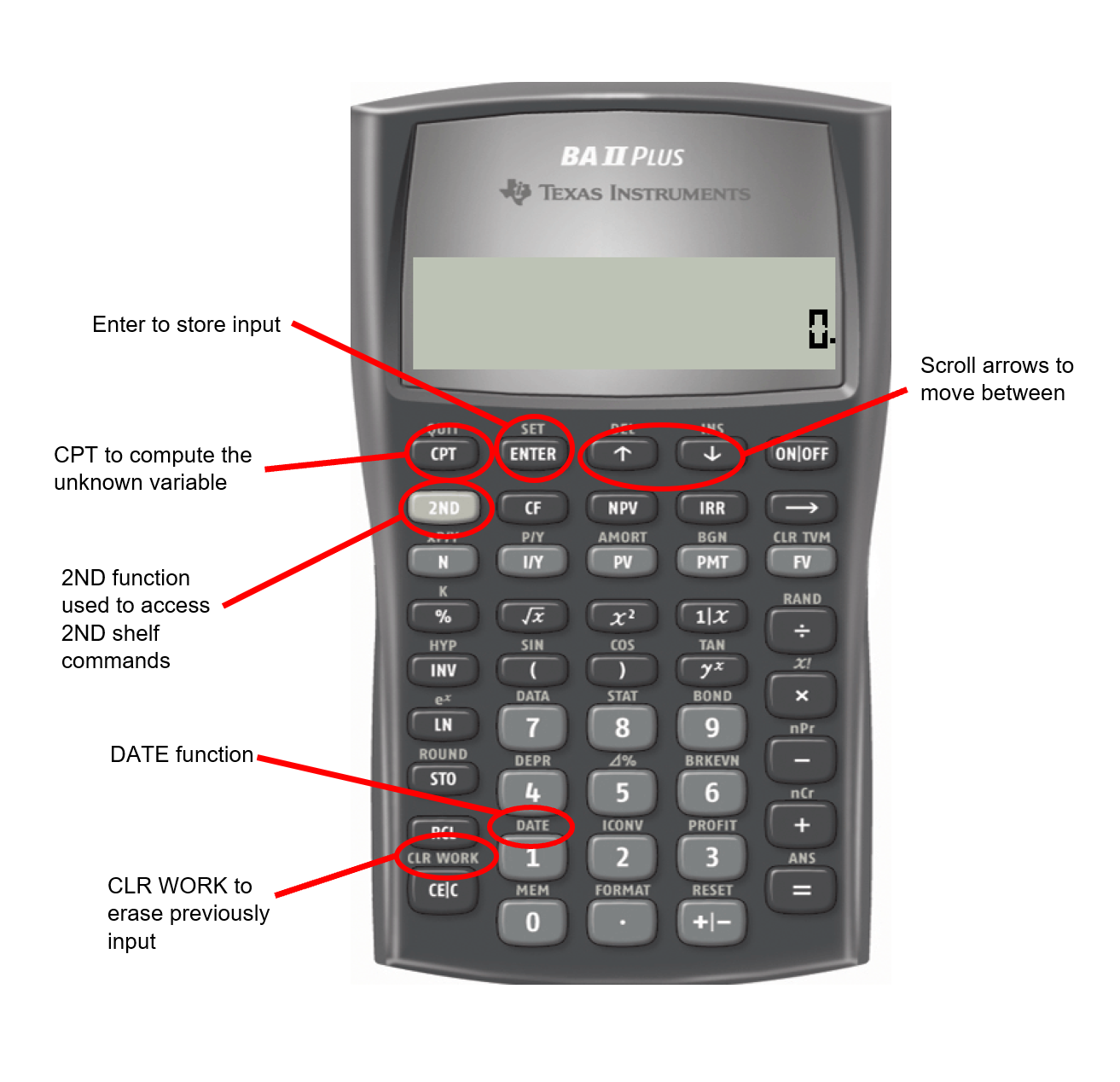

Using The BA 2+ Plus Date Function to Calculate the Exact Number of Days

In the video below we’ll demonstrate how to use the BA2+ Date Function.

When solving for t, decimals may appear in your solution. For example, if calculating t in days, the answer may show up as 45.9978 or 46.0023 days; however, interest is calculated only on complete days. This occurs because the interest amount (I) used in the calculation has been rounded off to two decimals. Since the interest amount is imprecise, the calculation of t is imprecise. When this occurs, round t off to the nearest integer.

Example 8.1.4: Time Using Dates

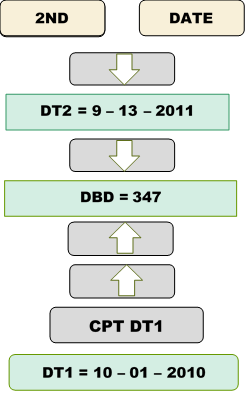

On September 13, 2011, Aladdin decided to pay back the Genie on his loan of $15,000 at 9% simple interest. If he paid the Genie the principal plus $1,283.42 of interest, on what day did he borrow the money from the Genie?

Solution:

Step 1: Given variables:

P = $15,000; I = $1,283.42; r = 9% per year; End Date = September 13, 2011

Step 2: The time is in days, but the rate is annual. Convert the rate to a daily rate;

Step 3: Solve for the time, t

Step 4: Use the DATE function to calculate the start date (DT1). Use the time in days.

Calculator Instructions

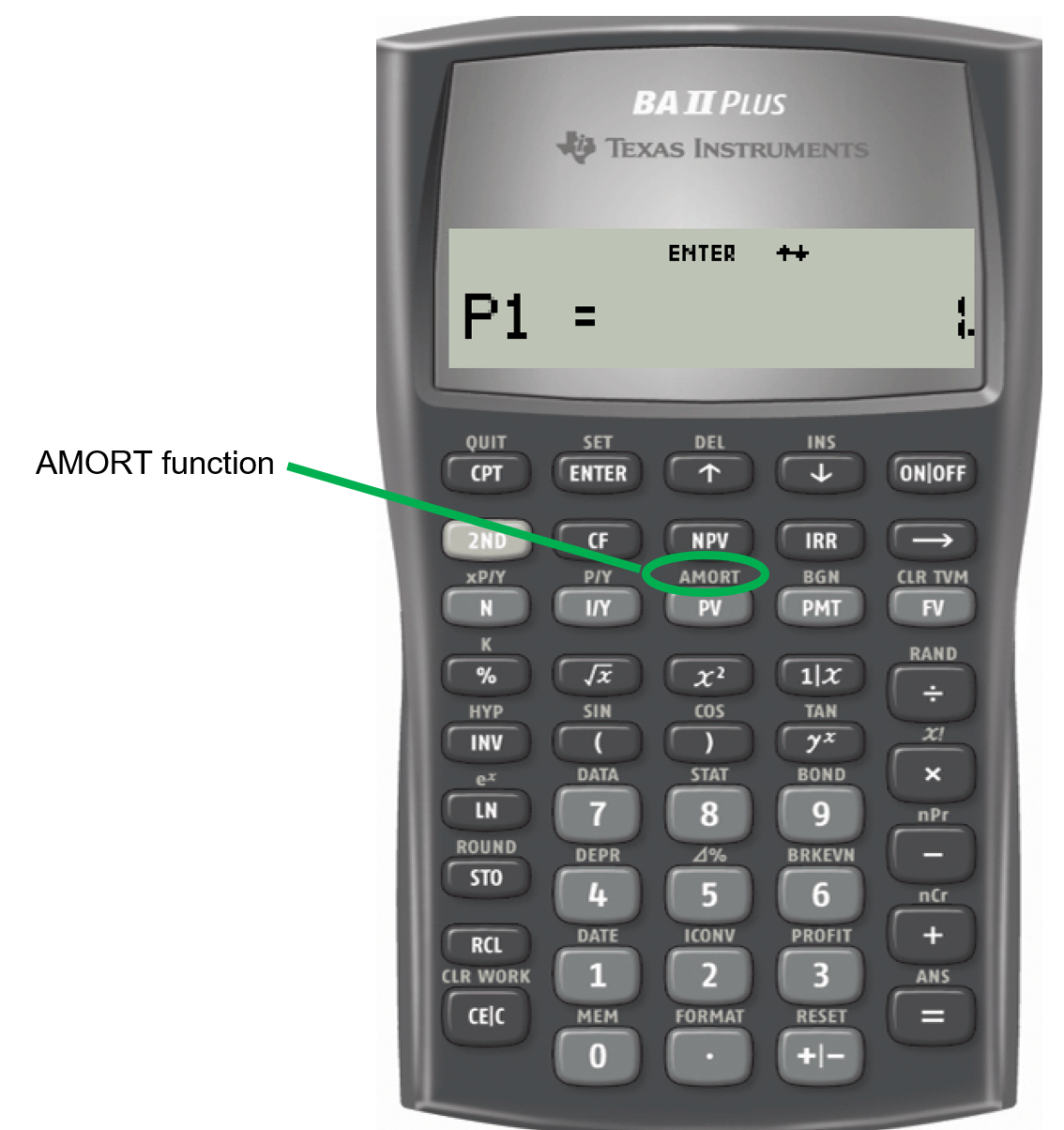

Figure 8.1.4: Calculator Intructions for Date Function [Image Description]

If Aladdin owed the Genie $1,283.42 of simple interest at 9% on a principal of $15,000, he must have borrowed the money 347 days earlier, which is October 1, 2010.

Exercises

In each of the exercises that follow, try them on your own. Full solutions are available should you get stuck.

Brynn borrowed $25,000 at 1% per month from a family friend to start her entrepreneurial venture on December 2, 2011. If she paid back the loan on June 16, 2012, how much simple interest did she pay? (Answer: 1,619.18)

If $6,000 principal plus $132.90 of simple interest was withdrawn on August 14, 2011, from an investment earning 5.5% interest, on what day was the money invested? (Answer: March 20, 2011)

Figure 8.1.1: Timeline showing PV =$1,100 at the Start with an arrow pointing to the end (right) where I = ? when t=5 months. r = 5% annually [Back to Figure 8.1.1]

Figure 8.1.2: Timeline showing PV = ? at the Start with an arrow pointing to the end (right) where I = $2,035 when t=11 months. r = 6% annually [Back to Figure 8.1.2]

Figure 8.1.3: Timeline showing PV =$95,000 at the Start with an arrow pointing to the end (right) where I = $1,187.50 when t=?. r = 5% annually [Back to Figure 8.1.3]

Figure 8.1.4: Calculator Instructions to use the Date Function. Instructions are: 2ND DATE, Down Arrow, DT2 = 9-13-2011, Down Arrow, DBD = 347, Up Arrow, Up Arrow, CPT DT1, DT1 = 10-01-2010 [Back to Figure 8.1.4]

8.2: Moving Money Involving Simple Interest

2

Moving Money Involving Simple Interest

Maturity Value (or Future Value)

The maturity value of a transaction is the amount of money resulting at the end of a transaction, an amount that includes both the interest and the principal together. It is called a maturity value because in the financial world the termination of a financial transaction is known as the “maturing” of the transaction. The amount of principal with interest at some point in the future, but not necessarily the end of the transaction, is known as the future value.

For any financial transaction involving simple interest, the following is true:

\[\mbox{Amount of money at the end} =\mbox{Amount of money at the beginning}\; +\;\mbox{Interest}\]

Applying algebra, you can summarize this expression by the following equation, where the future value or maturity value is commonly denoted by the symbol S.

\[S = P + I\]

Substituting in I=Prt">, yields the equation

\[S=P + Prt\]

or

\[S=P(1+rt)\]

The Formula

where,

I is Interest Amount. The interest amount is the dollar amount of interest that is paid or received.

P is Present Value or Principal. The present value is the amount borrowed or invested at the beginning of a period.

r is Simple Interest Rate. The interest rate is the rate of interest that is charged or earned during a specified time period. It is expressed as a percent.

t is Time Period. The time period or term is the length of the financial transaction for which interest is charged or earned.

From the future value formula S=P(1+rt) you can derive the present value formula (P):

Sometimes you will be required to calculate the simple interest dollar amount (I). the formula is given below.

Example 8.2.1: Calculating Maturity Value and Interest Amount

Assume that today you have $10,000 that you are going to invest at 7% simple interest for 11 months. How much money will you have in total at the end of the 11 months? How much interest do you earn?

Solution:

Step 1: Given variables:

P = $10,000; r = 7%; t = 11 months

Step 2: Express the time in years to match the annual rate;

Step 3: Solve for the future value, S.

This is the total amount after 11 months.

Step 4: Solve for the interest amount, I.

I = $10,641.67 – $10,000.00 = $641.67

The $10,000 earns $641.67 in simple interest over the next 11 months, resulting in $10,641.67 altogether.

Example 8.2.2: Saving for a Down Payment on a Home

You just inherited $35,000 from your uncle’s estate and plan to purchase a house four months from today. If you use your inheritance as your down payment on the house, how much will you be able to put down if your money earns 4¼% simple interest? How much interest will you have earned?

Solution:

Calculate the amount of money four months from now including both the principal and interest earned. This is the maturity value (S). Also calculate the interest earned (I).

Step 1: Given variables:

P = $35,000; t = 4months; per year

Step 2: Express the time in years to match the annual rate;

Four months from now you will have $35,495.83 as a down payment toward your house, which includes $35,000 in principal and $495.83 of interest.

Example 8.2.3: Saving for Tuition

Recall the section opener, where you needed $8,000 for tuition in the fall and the best simple interest rate you could find was 4.5%. Assume you have eight months before you need to pay your tuition. How much money do you need to invest today?

Solution:

Calculate the principal amount of money today that you must invest such that it will earn interest and end up at the $8,000 required for the tuition.

Step 1: Given variables:

S = $8,000; r=4.5% per year; t = 8 months

Step 2: Express the time in years to match the annual rate;

If you place $7,766.99 into the investment, it will grow to $8,000 in the eight months.

Example 8.2.4: What Exactly Are You being Offered?

You are sitting in an office at your local financial institution on August 4. The bank officer says to you, “We will make you a great deal. If we advance that line of credit and you borrow $20,000 today, when you want to repay that balance on September 1 you will only have to pay us $20,168.77, which is not much more!” Before answering, you decide to evaluate the statement. Calculate the simple interest rate that the bank officer used in her calculations.

Solution:

Determine the rate of interest that you would be charged on your line of credit.

Step 1: Given variables:

P = $20,000; S = $20,168.77; t = August 4 to September 1

Step 2: Calculate the number of days in the transaction.

Calculator Instructions:

Assume the year 2011 and use the DATE function to find the exact number of days:

Table 8.2.1. Calculator Inputs for Example 8.2.4

DT1

DT2

DBD</th

Mode

8.0411

9.0111

Answer: 28

ACT

Step 3: Since interest rates are usually expressed annually, convert the time from days to an annual number;

Step 4: Calculate the amount of interest, I.

Step 5: Solve for r.

The interest rate on the offered line of credit is 11.0002% (note that it is probably exactly 11%; the extra 0.0002% is most likely due to the rounded amount of interest used in the calculation).

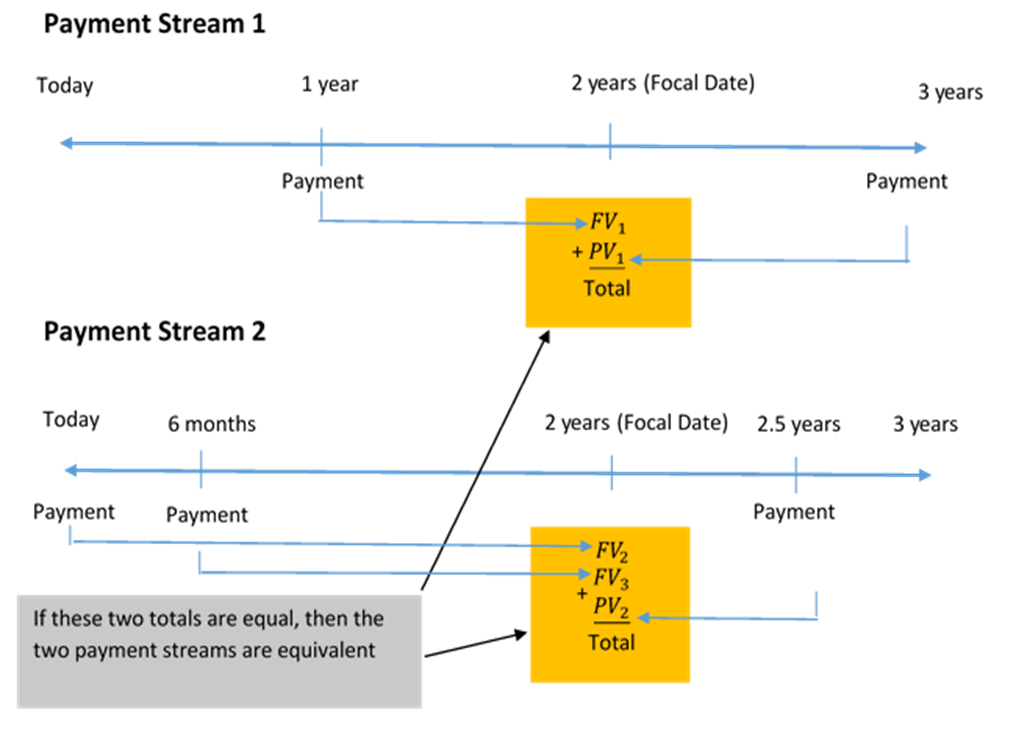

Equivalent Payments

Late Payments. If a debt is paid late, then a financial penalty that is fair to both parties involved should be imposed. That penalty should reflect a current rate of interest and be added to the original payment. Assume you owe $100 to your friend and that a fair current rate of simple interest is 10%. If you pay this debt one year late, then a 10% late interest penalty of $10 should be added, making your debt payment $110. This is no different from your friend receiving the $100 today and investing it himself at 10% interest so that it accumulates to $110 in one year.

Early Payments. If a debt is paid early, there should be some financial incentive (otherwise, why bother?). Therefore, an interest benefit, one reflecting a current rate of interest on the early payment, should be deducted from the original payment. Assume you owe your friend $110 one year from now and that a fair current rate of simple interest is 10%. If you pay this debt today, then a 10% early interest benefit of $10 should be deducted, making your debt payment today $100. If your friend then invests this money at 10% simple interest, one year from now he will have the $110, which is what you were supposed to pay.

Notice in these examples that a simple interest rate of 10% means $100 today is the same thing as having $110 one year from now. This illustrates the concept that two payments are equivalent payments if, once a fair rate of interest is factored in, they have the same value on the same day. Thus, in general you are finding two amounts at different points in time that have the same value, as illustrated in the figure below.

The steps required to calculate an equivalent payment are no different from those for single payments. If an early payment is being made, then you know the future value, so you solve for the present value (which removes the interest). If a late payment is being made, then you know the present value, so you solve for the future value (which adds the interest penalty).

Example 8.2.5: Making a Late Payment

Erin owes Charlotte $1,500 today. Unfortunately, Erin had some unexpected expenses and is unable to make her debt payment. After discussing the issue, they agree that Erin can make the payment nine months late and that a fair simple interest rate on the late payment is 5%. Use 9 months from now as your focal date and calculate how much Erin needs to pay. What is the amount of her late penalty?

Solution:

A late payment is a future value amount (S). The late penalty is equal to the interest (I).

Step 1: Given variables:

P = $1,500; r = 5% annually; t = 9 months

Step 2: Express the time in years to match the annual rate;

Erin’s late payment is for $1,556.25, which includes a $56.25 interest penalty for making the payment nine months late.

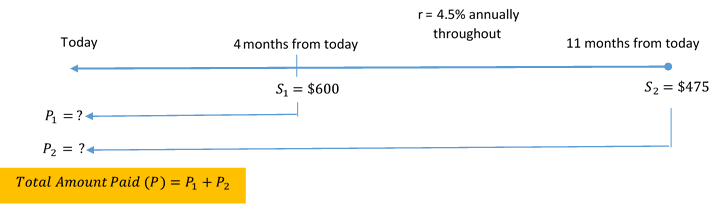

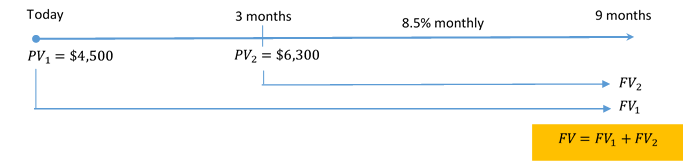

Example 8.2.6: Making an Early Payment

Rupert owes Aminata two debt payments: $600 four months from now and $475 eleven months from now. Rupert came into some money today and would like to pay off both of the debts immediately. Aminata has agreed that a fair interest rate is 7%. Using today as a focal date, what amount should Rupert pay? What is the total amount of his early payment benefit?

Solution:

An early payment is a present value amount (). Both payments will be moved to today and summed. The early payment benefit will be the total amount of interest removed ().

Step 1: Given variables:

The two payments and payment due dates are known.

Payment #1: S1 = $600; t = 4 months from now Payment #2: S2 = $475; t = 11 months from now

Replacement payment is being made today (the focal date).

Payment #1:

Step 2: Express the time in years to match the annual rate;

To clear both debts today, Rupert pays $1,032.68, which reflects a $42.32 interest benefit reduction for the early payment.

Exercises

In each of the exercises that follow, try them on your own. Full solutions are available should you get stuck.

An accountant needs to allocate the principal and simple interest on a loan payment into the appropriate ledgers. If the amount received was $10,267.21 for a loan that spanned April 14 to July 31 at 9.1%, how much was the principal and how much was the interest?(Answers: P = $9,998, I = $269.21)

Suppose Robin borrowed $3,600 on October 21 and repaid the loan on February 21 of the following year. What simple interest rate was charged if Robin repaid $3,694.63? (Answer: 7.80%)

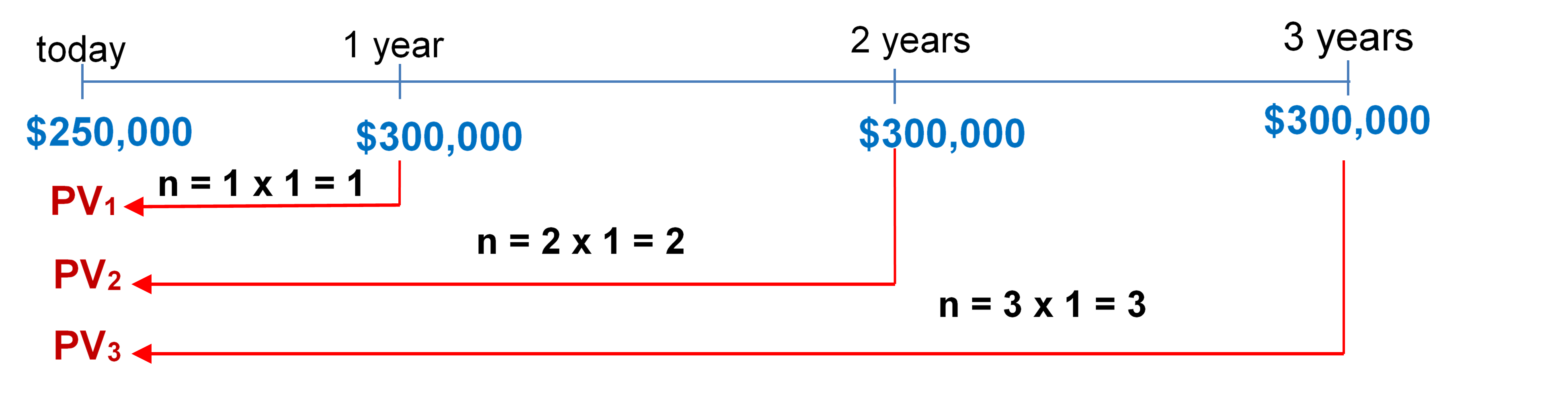

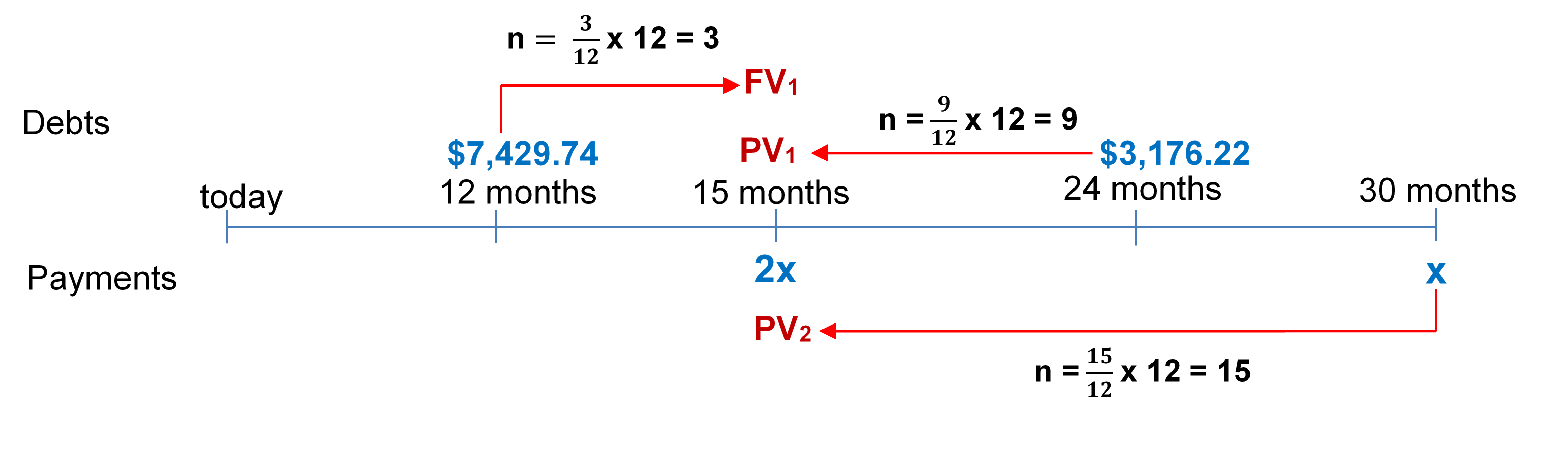

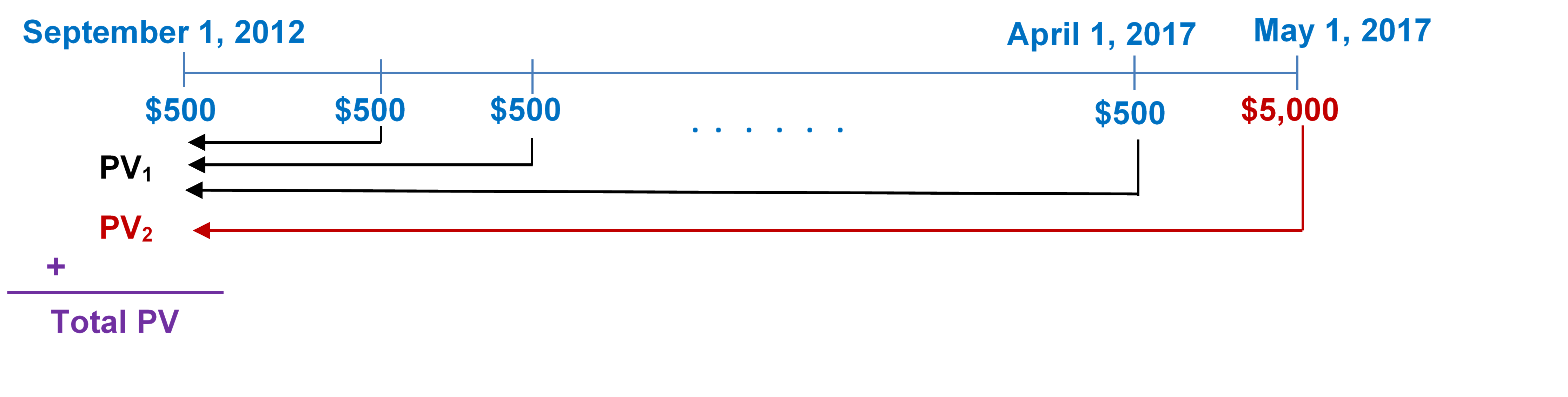

Jayne needs to make three payments to Jade requiring $2,000 each 5 months, 10 months, and 15 months from to day. She proposes instead making a single payment eight months from today. If Jade agrees to a simple interest rate of 9.5%, what amount should Jayne pay? (Answer: $5,911.32)

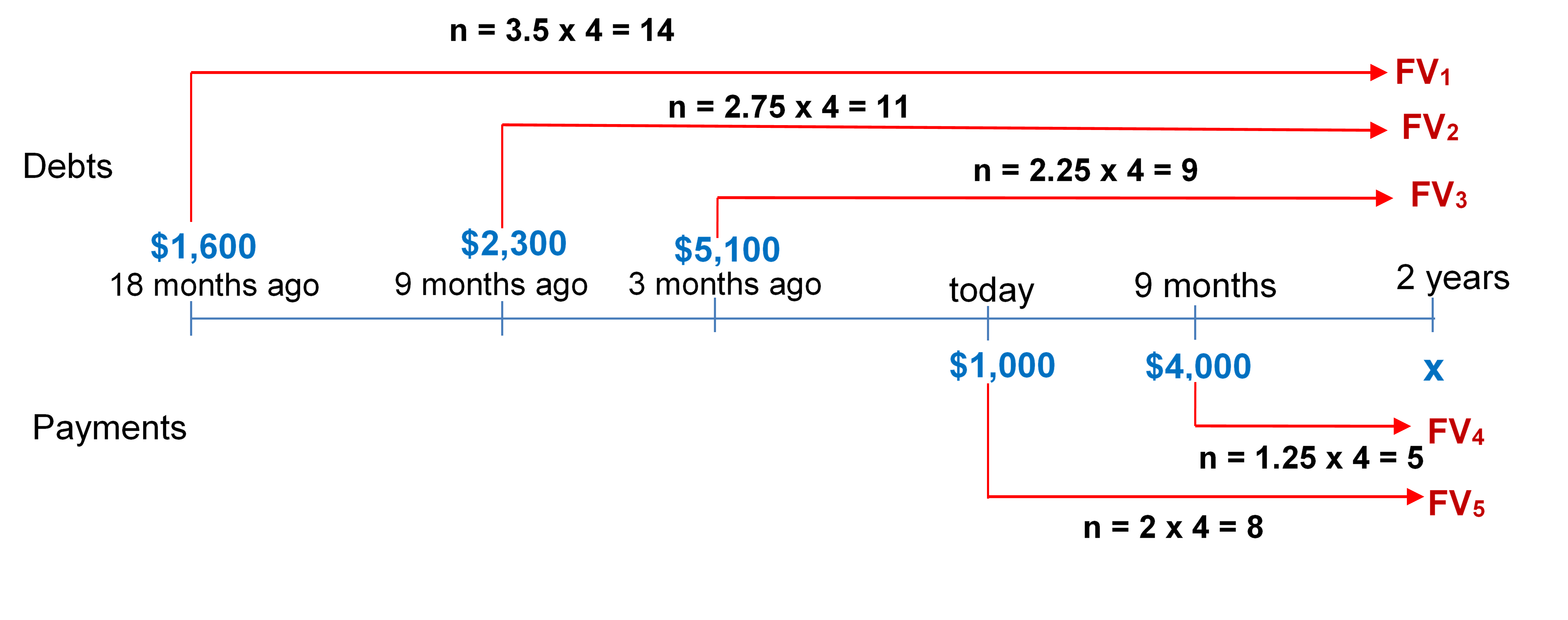

Merina is scheduled to make two loan payments to Bradford in the amount of $1,000 each, two months and nine months from now. Merina doesn’t think she can make those payments and offers Bradford an alternative plan where she will pay $775 seven months from now and another payment seven months later. Bradford determines that 8.5% is a fair interest rate. What is the amount of the second payment? (Answer: $1,306.99)

Figure 8.2.2: Timeline showing PV =$35,000 at Today (on the Left) with an arrow pointing to the end (on the Right) (4 months) where S = ? and r = 4.25% annually [Back to Figure 8.2.2]

Figure 8.2.3: Timeline showing S = $8,000 the end (on the Right) (8 months) with an arrow pointing back to Today (on the Left) where PV =? and r = 4.5% annually. [Back to Figure 8.2.3]

Figure 8.2.E: General Timeline for Equivalent Payments: On the left, “Earlier Date”, “We are trying to find the amount here…”. In the middle, “…at same fair rate of simple interest…”. At the end, “Later Date”, “that is equivalent to some amount over here.” [Back to Figure 8.2.E]

Figure 8.2.5: Timeline showing: On the Left: “Payment due today”, “P = $1,500”. On the Right: “Payment will be made 9 months later”, “S = ?”. r = 5% annually [Back to Figure 8.2.5]

Figure 8.2.6: Timeline showing S1 = $600 at 4 months from today and S2 = $475 at 11 months from today. S1 = $600 moves back to today as P1 = ? and S2 = $475 moves back to today as P2 = ?. At Today, Total Amount Paid (P) = P1 + P2. r = 4.5% annually throughout. [Back to Figure 8.2.6]

8.3: Savings Accounts And Short-Term GICs

3

Savings Accounts And Short Term GICs

Savings Accounts

A savings account is a deposit account that bears interest and has no stated maturity date. These accounts are found at most financial institutions, such as commercial banks (Royal Bank of Canada, TD Canada Trust, etc.), trusts (Royal Trust, Laurentian Trust, etc.), and credit unions (FirstOntario, Steinbach, Assiniboine, Servus, etc.). Owners of such accounts make deposits to and withdrawals from these accounts at any time, usually accessing the account at an automatic teller machine (ATM), at a bank teller, or through online banking.

A wide variety of types of savings accounts are available. This textbook focuses on the most common features of most savings accounts, including how interest is calculated, when interest is deposited, insurance against loss, and the interest rate amounts available.

How Interest Is Calculated. There are two common methods for calculating simple interest:

Accounts earn simple interest that is calculated based on the daily closing balance of the account. The closing balance is the amount of money in the account at the end of the day. Therefore, any balances in the account throughout a single day do not matter. For example, if you start the day with $500 in the account and deposit $3,000 at 9:00 a.m., then withdraw the $3,000 at 4:00 p.m., your closing balance is $500. That is the principal on which interest is calculated, not the $3,500 in the account throughout the day.

Accounts earn simple interest based on a minimum monthly balance in the account. For example, if in a single month you had a balance in the account of $900 except for one day, when the balance was $500, then only the $500 is used in calculating the entire month’s worth of interest. When Interest Is Deposited. Interest is accumulated and deposited (paid) to the account once monthly, usually on the first day of the month. Thus, the interest earned on your account for the month of January appears as a deposit on February 1.

Insurance against Loss. Canadian savings accounts at commercial banks are insured by the national Canada Deposit Insurance Corporation (CDIC), which guarantees up to $100,000 in savings. At credit unions, this insurance is usually provided provincially by institutions such as the Deposit Insurance Corporation of Ontario (DICO), which also guarantees up to $100,000. This means that if your bank were to fold, you could not lose your money (so long as your deposit was within the maximum limit). Therefore, savings accounts carry almost no risk.

Interest Rate Amounts. Interest rates are higher for investments that are riskier. Savings accounts carry virtually no risk, which means the interest rates on savings accounts tend to be among the lowest you can earn. At the time of writing, interest rates on savings accounts ranged from a low of 0.05% to a high of 1.95%. Though this is not much, it is better than nothing and certainly better than losing money!

While a wide range of savings accounts are available, these accounts generally follow one of two common structures when it comes to calculating interest. These structures are flat rate savings accounts and tiered savings accounts. Each of these is discussed separately.

How It Works

Flat-Rate Savings Accounts.

A flat-rate savings account has a single interest rate that applies to the entire balance. The interest rate may fluctuate in sync with short-term interest rates in the financial markets.

Follow these steps to calculate the monthly interest for a flat-rate savings account:

Step 1: Identify the interest rate, opening balance, and the monthly transactions in the savings account.

Step 2: Set up a flat-rate table as illustrated here. Create a number of rows equaling the number of monthly transactions (deposits or withdrawals) in the account plus one.

Table 8.3.1. Example of a Flat-Rate Table for Step 2

Date

Closing Balance in Account

# of Days

Simple Interest Earned

Total Interest earned

Step 3: For each row of the table, set up the date ranges for each transaction and calculate the balance in the account for each date range.

Step 4: Calculate the number of days that the closing balance is maintained for each row.

Step 5: Apply simple interest formula I = Prt, to each row in the table. Ensure that rate and time are expressed in the same units. Do not round off the resulting interest amounts (I).

Step 6: Sum the Simple Interest Earned column and round off to two decimals.

When you are calculating interest on any type of savings account, pay careful attention to the details on how interest is calculated and any restrictions or conditions on the balance that is eligible to earn the interest.

Example 8.3.1: Savings at the Royal Bank

The RBC High Interest Savings Account pays 0.75% simple interest on the daily closing balance in the account and the interest is paid on the first day of the following month. On March 1, the opening balance in the account was $2,400. On March 12, a deposit of $1,600 was made. On March 21, a withdrawal of $2,000 was made. Calculate the total simple interest earned for the month of March.

Solution:

Calculate the total interest amount (I) for the month.

Step 1: Given variables:

r = 0.75% per year

The following transactions dates are known.

March 1 opening balance = $2,400 March 12 deposit = $1,600 March 21 withdrawal = $2,000

Step 2: Set up a flat-rate table.

Step 3: Determine the date ranges for each balance throughout the month and calculate the closing balances.

Step 4: For each row of the table, calculate the number of days involved.

Step 5: Apply simple interest formula I = Prt to calculate simple interest on each row.

Step 6: Sum the Simple Interest Earned.

Table 8.3.2. Flat-Rate Table for Savings at the Royal Bank Example 8.3.1

For the month of March, the savings account earned a total simple interest of $1.73, which was deposited to the account on April 1.

Exercise: Savings Accounts

In the exercise that follow, try it on your own. Full solution is available should you get stuck.

Canadian Western Bank offers a Summit Savings Account with posted interest rates as indicated in the table below. Only each tier is subject to the posted rate, and interest is calculated daily based on the closing balance.

Table 8.3.3. Interest Rates for Summit Savings Account

Balance

Interest Rate

$0 – $5,000.00

0%

$5,000.01 – $1,000,000.00

1.05%

$1,000,000.01 and up

0.80%

December’s opening balance was $550,000. Two deposits in the amount of $600,000 each were made on December 3 and December 21. Two withdrawals in the amount of $400,000 and $300,000 were made on December 13 and December 24, respectively. What interest for the month of December will be deposited to the account on January 1? (Answer: $868.55)

A tiered savings account pays higher rates of interest on higher balances in the account. This is very much like a graduated commission on gross earnings. For example, you might earn 0.25% interest on the first $1,000 in your account and 0.35% for balances over $1,000. Most of these tiered savings accounts use a portioning system. This means that if the account has $2,500, the first $1,000 earns the 0.25% interest rate and it is only the portion above the first $1,000 (hence, $1,500) that earns the higher interest rate.

How It Works

Follow these steps to calculate the monthly interest for a tiered savings account:

Step 1: Identify the interest rate, opening balance, and the monthly transactions in the savings account.

Step 2: Set up a tiered interest rate table as illustrated below. Create a number of rows equaling the number of monthly transactions (deposits or withdrawals) in the account plus one. Adjust the number of columns to suit the number of tiered rates. Fill in the headers for each tiered rate with the balance requirements and interest rate for which the balance is eligible.

Table 8.3.4. Example of a Tiered Interest Rate Table for Step 2

Dates

Closing Balance in Account

# of Days

Tier Rate #1 Balance Requirements and Interest Rate

Tier Rate #2 Balance Requirements and Interest Rate

Tier Rate #3 Balance Requirements and Interest Rate

Eligible P

I = Prt

Eligible P

I = Prt

Eligible P

I = Prt

Total Monthly Interest Earned

Step 3: For each row of the table, set up the date ranges for each transaction and calculate the balance in the account for each date range.

Step 4: For each row, calculate the number of days that the closing balance is maintained.

Step 5: Assign the closing balance to the different tiers, paying attention to whether portioning is being used. In each cell with a balance, apply simple interest formula I = Prt. Ensure that rate and time are expressed in the same units. Do not round off the resulting interest amounts (I).

Step 6: To calculate the Total Monthly Interest Earned, sum all interest earned amounts from all tier columns and round off to two decimals.

Example 8.3.2: A Rate Builder Tiered Account

The Rate Builder savings account at your local credit union pays simple interest on the daily closing balance as indicated in the table below:

Table 8.3.5. Balance and Corresponding Interest Rate for Rate Builder Savings Account

Balance

Interest Rate

$0.00 to $500.00

0% on entire balance

$500.01 to $2,500.00

0.5% on entire balance

$2,500.01 to $5,000.00

0.95% on this portion of balance only

$5,000.01 and up

1.35% on this portion of balance only

In the month of August, the opening balance on an account was $2,150.00. Deposits were made to the account on August 5 and August 15 in the amounts of $3,850.00 and $3,500.00. Withdrawals were made from the account on August 12 and August 29 in the amounts of $5,750.00 and $3,000.00. Calculate the simple interest earned for the month of August.

Solution:

Calculate the total interest amount (I) for the month of August.

Step 1: The interest rate structure is in the table above.

The transactions and dates are also known:

August 1 opening balance = $2,150.00

August 5 deposit = $3,850.00

August 12 withdrawal = $5,750.00

August 15 deposit = $3,500.00

August 29 withdrawal = $3,000.00

Step 2: Set up a tiered interest rate table with four columns for the tiered rates.

Step 3: Determine the date ranges for each balance throughout the month and calculate the closing balances.

Step 4: Calculate the number of days involved on each row of the table.

Step 5: Assign the closing balance to each tier accordingly. Apply Formula 8.1 to any cell containing a balance.

Step 6: Total up all of the interest from all cells of the table.

Table 8.3.6. Interest Calculated from Tiered Interest Table in Example 8.3.2

Calculations of Interest Based on Date with Total Interest Earned at the Bottom

Dates:Aug 1 to Aug 5

Closing Balance in Account: $2,150 # of Days: 5 – 1 = 4

0.5% $500.01 to $2,500 (Entire balance)

Dates: Aug 5 to Aug 12

Closing Balance in Account:$2,150 + $3,850= $6,000 # of Days: 12 – 5 = 7

0.5% $500.01 to $2,500 (Entire balance)

0.95% $2,500.01 to $5,000 (This portion only)

1.35% $5,000.01 and up (This portion only)

Dates: Aug 12 to Aug 15

Closing Balance in Account:$6,000 – $5,750 = $250 # of Days: 15 – 12 = 3

0% $0 to $500 (Entire balance)

Dates: Aug 15 to Aug 29

Closing Balance in Account:$250 + $3,500= $3,750 # of Days: 29 – 15 = 14

0.5% $500.01 to $2,500 (Entire balance)

0.95% $2,500.01 to $5,000 (This portion only)

Dates:Aug 29 to Sep 1

Closing Balance in Account:$3,750 – $3,000= $750 # of Days: 31 – 29 + 1 = 3

0.5% $500.01 to $2,500 (Entire balance)

Total Interest Earned

For the month of August, the tiered savings account earned a total simple interest of $2.04, which was deposited to the account on September 1.

A guaranteed investment certificate (GIC) is an investment that offers a guaranteed rate of interest over a fixed period of time. GICs are found mostly at commercial banks, trust companies, and credit unions. In this section, you will deal only with short-term GICs, defined as those that have a time frame of less than one year.

The table below summarizes three factors that determine the interest rate on a short-term GIC: principal, time, and redemption privileges.

Table 8.3.7. Factors Determining Interest Rates on Short-Term GICs

Factors Determining Interest Rate

Higher Interest Rates

Lower Interest Rates

Principal Amount

Large

Small

Time

Longer

Shorter

Redemption Privileges

Nonredeemable

Redeemable

Amount of Principal. Typically, a larger principal is able to realize a higher interest rate than a smaller principal.

Time. The length of time that the principal is invested affects the interest rate. Short-term GICs range from 30 days to 364 days in length. A longer term usually realizes higher interest rates.

Redemption Privileges. The two types of GICs are known as redeemable and nonredeemable. A redeemable GIC can be cashed in at any point before the maturity date, meaning that you can access your money any time you want it. A nonredeemable GIC “locks in” your money for the agreed-upon term. Accessing that money before the end of the term usually incurs a stiff financial penalty, either on the interest rate or in the form of a financial fee. Nonredeemable GICs carry a higher interest rate.

To summarize, if you want to receive the most interest it is best to invest a large sum for a long time in a nonredeemable short-term GIC.

How It Works

Short-term GICs involve a lump sum of money (the principal) invested for a fixed term (the time) at a guaranteed interest rate (the rate). Most commonly the only items of concern are the amount of interest earned and the maturity value. Therefore, you need the same four steps as for single payments involving simple interest shown in Section 8.2.

Example 8.3.3: GIC Choices

Your parents have $10,000 to invest. They can either deposit the money into a 364-day nonredeemable GIC at Assiniboine Credit Union with a posted rate of 0.75%, or they could put their money into back-to-back 182-day nonredeemable GICs with a posted rate of 0.7%. At the end of the first 182 days, they will reinvest both the principal and interest into the second GIC. The interest rate remains unchanged on the second GIC. Which option should they choose?

Solution:

For both options, calculate the future value (S), of the investment after 364 days. The one with the higher future value is your parents’ better option.

Step 1: Given variables:

For the first GIC investment option: P = $10,000; r = 0.75% per year; t = 364 days For the second GIC investment option: Initial P = $10,000; r = 0.7% per year; t = 182 days each

Step 2: The rate is annual, the time is in days. Convert the time to an annual number. Transforming both time variables, and

Step 3: (1st GIC option): Calculate the maturity value S1 of the first GIC option after its 364-day term.

Step 3: (2nd GIC option, 1st GIC): Calculate the maturity value S2 after the first 182-day term.

Step 3: (2nd GIC option, 2nd GIC): Reinvest the first maturity value as principal for another term of 182 days and calculate the final future value S3.

The 364-day GIC results in a maturity value of $10,074.79, while the two back-to-back 182-day GICs result in a maturity value of $10,069.93. Clearly, the 364-day GIC is the better option as it will earn $4.86 more in simple interest.

Exercises: Short Term GIC

In the exercise that follow, try it on your own. Full solution is available should you get stuck.

If you place $25,500 into an 80-day short-term GIC at TD Canada Trust earning 0.55% simple interest, how much will you receive when the investment

matures? (Answer: $25,530.74)

Interest rates in the GIC markets are always fluctuating be cause of changes in the short-term financial markets. If you have $50,000 to invest today, you could place the money into a 180-day GIC at Canada Life earning a fixed rate of 0.4%, or you could take two consecutive 90-day GICs. The current posted fixed rate on 90-day GICs at Canada Life is 0.3%. Trends in the short-term financial markets suggest that within the next 90 days short-term GIC rates will be rising. What does the short-term 90-day rate need to be 90 days from now to arrive at the same maturity value as the 180-day GIC? Assume that the entire maturity value of the first 90-day GIC would be reinvested. (Answer: 0.50%)

8.6: Application: Treasury Bills and Commercial Paper

4

Application: Treasury Bills and Commercial Paper

Treasury Bills: The Basics

Treasury bills, also known as T-bills, are short-term financial instruments that both federal and provincial governments issue with maturities no longer than one year. Approximately 27% of the national debt is borrowed through T-bills.

Here are some of the basics about T-bills:

The Government of Canada regularly places T-bills up for auction every second Tuesday. Provincial governments issue them at irregular intervals.

The most common terms for federal and provincial T-bills are 30 days, 60 days, 90 days, 182 days, and 364 days.

T-bills do not earn interest. Instead, they are sold at a discount and redeemed at full value. This follows the principle of “buy low, sell high.” The percentage by which the value of the T-bill grows from sale to redemption is called the yield or rate of return. From a mathematical perspective, the yield is calculated in the exact same way as an interest rate is calculated, and therefore the yield is mathematically substituted as the discount rate in all simple interest formulas. Up-to-date yields on T-bills can be found at www.bankofcanada.ca/en/rates/monmrt.html.

The face valueof a T-bill (also called par value) is the maturity value, payable at the end of the term. It includes both the principal and yield together.

T-bills do not have to be retained by the initial investor throughout their entire term. At any point during a T-bill’s term, an investor is able to sell it to another investor through secondary financial markets. Prevailing yields on T-bills at the time of sale are used to calculate the price.

Commercial Papers – The Basics

A commercial paper (or paper for short) is the same as a T-bill except that it is issued by a large corporation instead of a government. It is an alternative to short-term bank borrowing for large corporations. Most of these large companies have solid credit ratings, meaning that investors bear very little risk that the face value will not be repaid upon maturity.

Commercial papers carry the same properties as T-bills. The only fundamental differences lie in the term and the yield:

The terms are usually less than 270 days but can range from 30 days to 364 days. The most typical terms are 30 days, 60 days, and 90 days.

The yield on commercial papers tends to be slightly higher than on T-bills since corporations do carry a higher risk of default than governments.

How It Works

Mathematically, T-bills and commercial papers operate in the exact same way. The future value for both of these investment instruments is always known since it is the face value. Commonly, the two calculated variables are either the present value (price) or the yield (interest rate). The yield is explored later in this section. Follow these steps to calculate the price:

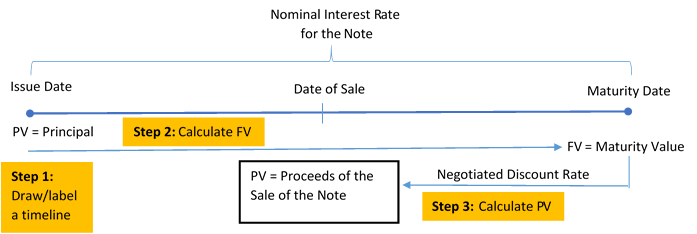

Step 1: The face value, yield, and time before maturity must be known. Draw a timeline if necessary, as illustrated below, and identify the following:

The face value (S).

The yield (r) on the date of the sale, which is always expressed annually. Remember that mathematically the yield is the same as the discount rate.

The number of days (t">t) remaining between the date of the sale and the maturity date. Count the first day but not the last day. Express the number of days annually to match the annual yield.

Figure 8.6.0: General Timeline for T-Bills and Commercial Papers [Image Description]

Step 2: Solve for the present value. using, which is the price of the T-bill or commercial paper. This price is always less than the face value.

A Government of Canada 182-day issue T-bill has a face value of $100,000. Market yields on these T-bills are 1.5%. Calculate the price of the T-bill on its issue date.

Solution:

Step 1: Given variables:

S = $100,000; r = 1.5% ; t = 182/365

Step 2: Solve for the present value, P.

An investor will pay $99,257.61 for the T-bill. If the investor holds onto the T-bill until maturity, the investor realizes a yield of 1.5% and receives $100,000.

Example 8.6.2: Selling a Commercial Paper During Its Term

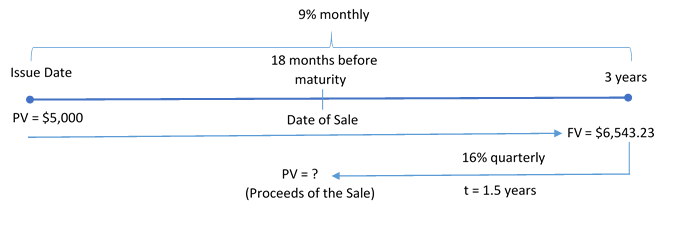

Pfizer Inc. issued a 90-day, $250,000 commercial paper on April 18 when the market rate of return was 3.1%. The paper was sold 49 days later when the market rate of return was 3.63%. Calculate the price of the commercial paper on its date of sale.

Solution:

Note that the historical rate of return of 3.1% is irrelevant to the price of the commercial paper today. The number of days elapsed since the date of issue is also unimportant. The number of days before maturity is the key piece of information.

S = $250,000; r = 3.63%; t = 90 – 49 = 41 days or 41/365 years

Step 2:Solve for the present value, P.

An investor pays $248,984.76 for the commercial paper on the date of sale. If the investor holds onto the commercial paper for 41 more days (until maturity), the investor realizes a yield of 3.63% and receives $250,000.

How It Works

Calculating a Rate of Return: Sometimes the unknown value when working with T-bills and commercial papers is the yield, or rate of return. In these cases, follow these steps to solve the problem:

Step 1: The face value, price, and time before maturity must be known. Draw a timeline if necessary, as illustrated below, and identify:

The number of days (t) remaining between the date of the sale and the maturity date. Count the first day but not the last day. Express the number of days annually so that the calculated yield will be annual.

Step 2: Apply formula I = S − P, to calculate the interest earned during the investment.

Step 3: Apply simple interest formula, I=Prt, rearranging for r to solve for the interest rate (or yield or rate of return).

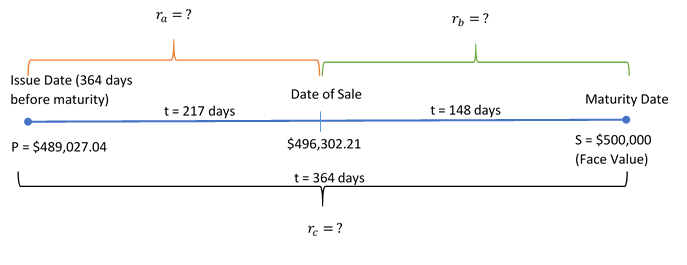

Example 8.6.3: Figuring Out Rates of Return for Multiple Investors

Marlie paid $489,027.04 on the date of issue for a $500,000 face value T-bill with a 364-day term. Marlie received $496,302.21 when he sold it to Josephine 217 days after the date of issue. Josephine held the T-bill until maturity. Determine the following:

a) Marlie’s actual rate of return. b) Josephine’s actual rate of return. c) If Marlie held onto the T-bill for the entire 364 days instead of selling it to Josephine, what would his rate of return have been? d) Comment on the answers to (a) and (c).

Solution:

Calculate three yields or rates of return (r) involving Marlie and the sale to Josephine, Josephine herself, and Marlie without the sale to Josephine. Afterwards, comment on the rate of return for Marlie with and without the sale.

When Marlie sold the T-bill after holding it for 217 days, he realized a 2.50% rate of return. Josephine then held the T-bill for another 148 days to maturity, realizing a 1.85% rate of return. If Marlie hadn’t sold the note to Josephine and instead held it for the entire 364 days, he would have realized a 2.25% rate of return.

Step 4: Compare the answers for (a) and (c) and comment.

The yield on the date of issue was 2.25%. Marlie realized a higher rate of return because the interest rates in the market decreased during the 217 days he held it (to 1.85%, which is what Josephine is able to obtain by holding it until maturity). This raises the selling price of the T-bill. If his investment of $489,027.04 grows by 2.25% for 217 days, he has $6,541.57 in interest. The additional $733.60 of interest (totaling $7,275.17) is due to the lower yield in the market, increasing his rate of return to 2.50% instead of 2.25%.

Exercises

In each of the exercises that follow, try them on your own. Full solutions are available should you get stuck.

A 60-day, $90,000 face value commercial paper was issued when yields were 2.09%. What was its purchase price? (Answer: $89,691.85)

A 90-day Province of Ontario T-bill with a $35,000 face value matures on December 11. Farrah works for Hearthplace Industries and notices that the company temporarily has some extra cash available. If she invests the money on October 28, when the yield is 4.94%, and sells the T-bill on November 25, when the yield is 4.83%, calculate how much money Farrah earned and the rate of return she realized. (Answer: Amount earned = $133.24; r = 4.99%)

Philippe purchased a $100,000 Citicorp Financial 220-day commercial paper for $96,453.93. He sold it 110 days later to Damien for $98,414.58, who then held onto the commercial paper until its maturity date. a) What is Philippe’s actual rate of return? (Answer: 6.74%)

b) What is Damien’s actual rate of return? (Answer: 5.35%)

c) What is the rate of return Philippe would have realized if he had held onto the note instead of selling it to Damien? (Answer: 6.10%)

Figure 8.6.0: Timeline showing on the Left, “Date of sale”, “P = ?”, with arrow moving to the end (on the Right) to “Maturity Date” and “S = Face Value”. Yield (r) on the Date of Sale. [Back to Figure 8.6.0]

Figure 8.6.2: Timeline showing “Maturity Date” on the Right with arrow back to the Left to “90 Days Before Maturity (Date of Issue)”. At “Maturity Date”, S = $250,000 moves back to “49 Days After Date of Issue” to P = ? with r = 3.63% annually. [Back to Figure 8.6.2]

Figure 8.6.Y: Timeline showing on the Left, “Date of sale”, “P = Price”. On the Right, “Maturity Date” and “S = Face Value”. in the Middle, “On Date of Sale”, “Yield (r) = ? annually”. [Back to Figure 8.6.Y]

Figure 8.6.3: Timeline showing on the Left, “Issue Date (364 days before maturity)”, “P = $489,027.04”. t = 217 days later to “Date of Sale” and “$496,302.21”. t = 148 days later to “Maturity Date” and “S = $500,000 (Face Value)” on the Right. ra = ? from Issue Date until Date of Sale. rb = ? from Date of Sale to Maturity Date. rc = ? and t = 364 days from Issue Date until Maturity Date. [Back to Figure 8.6.3]

Enter two of the three variables (DT1, DT2, DBD) by pressing Enter after each input and using and to scroll through the display. The variables are:

DT1 = The starting date of the transaction

DT2 = The ending date of the transaction

DBD = The days between the dates, counting the first day but not the last, which is the time period of the transaction.

ACT / 360 = A setting for determining how the calculator determines the DBD. In Canada, you should maintain this setting on ACT, which is the actual number of days. In other countries, such as the United States, they treat each year as having 360 days (the 360 setting) and each month as having 30 days. If you need to toggle this setting, press 2nd SET.

Enter all dates in the format of MM.DDYY, where MM is the numerical month, DD is the day, and YY is the last two digits of the year. DD and YY must always be entered with both digits.

Press CPT on the unknown (when it is on the screen display) to compute the answer.

Image Description

Figure 8.C: Picture of the BAII Plus calculator showing the “ENTER”, “CPT”, “2ND”, “DATE”, “CLR WORK”, “UP ARROW”, “DOWN ARROW” keys. [Back to Figure 8.C]

Chapter 8: Glossary of Terms

9

Glossary of Terms

Accrued interest Commercial paper Compound interest Current balance Discount rate Equivalent payments Face value of a T-bill Fixed interest rate Future value Guaranteed investment certificate (GIC) Interest amount Interest rate Maturity date Maturity value Present value Principal Repayment schedule Savings account Simple interest Time period Treasury bills Variable interest rate Yield

Chapter 9

II

Learning Objectives

Differentiate between the concept of compound interest and simple interest.

Calculate the future value and present value of investments and loans in compound interest applications using both the algebraic and financial calculator methods.

Calculate equivalent payments that replace another payment or a set of payments.

Calculate the effective and equivalent interest rates for nominal interest rates.

Calculate periodic and nominal interest rates.

Calculate the number of compounding periods and time period of an investment or loan.

9.1: Compound Interest and Fundamentals

10

Compound Interest and Fundamentals

Compound interest is used for most transactions lasting one year or more. In simple interest, interest is converted to principal at the end of the transaction. Therefore, all interest is based solely on the original principal amount of the transaction. Compound interest, by contrast, involves interest being periodically converted to principal throughout a transaction, with the result that the interest itself also accumulates interest.

Calculating the Periodic Interest Rate

The first step in learning about investing or borrowing under compound interest is to understand the interest rate used in converting interest to principal. You commonly need to convert the posted interest rate to find the exact rate of interest earned or charged in any given time period.

Nine percent compounded monthly is equal to a periodic interest rate of 0.75% per month. This means that interest is converted to principal 12 times throughout the year at the rate of 0.75% each time.

b)

Six percent compounded quarterly is equal to a periodic interest rate of 1.5% per quarter. This means that interest is converted to principal 4 times (every three months) throughout the year at the rate of 1.5% each time.

Example 9.1.2: The Nominal Interest Rate (I/Y)

Calculate the nominal interest rate, I/Y, for the following periodic interest rates:

a) per month b) 0.05% per day

Solution:

Step 1: Given information:

a) ; C/Y = monthly =12 times per year b) i = 0.05%; C/Y = daily = 365 times per year

Step 2: For each question, apply the periodic interest formula and rearrange for the nominal rate, I/Y.

a)

A periodic interest rate of per month is equal to a nominal interest rate of 7% compounded monthly.

b)

A periodic interest rate of 0.05% per day is equal to a nominal interest rate of 18.25% compounded daily.

Example 9.1.3: Compounds per Year (C/Y)

Calculate the compounding frequency (C/Y) for the following nominal and periodic interest rates:

Step 2: For each question, apply the periodic interest formula and rearrange for the compounding frequency, C/Y.

a)

For the nominal interest rate of 6% to be equal to a periodic interest rate of 3%, the compounding frequency must be twice per year, which means a compounding period of every six months, or semi-annually.

b)

For the nominal interest rate of 9% to be equal to a periodic interest rate of 2.25%, the compounding frequency must be four times per year, which means a compounded period of every three months, or quarterly.

Exercises

In each of the exercises that follow, try them on your own. Full solutions are available should you get stuck.

Calculate the periodic interest rate if the nominal interest rate is 7.75% compounded monthly. (Answer: 0.65%)

Calculate the compounding frequency for a nominal interest rate of 9.6% if the periodic interest rate is 0.8%.(Answer: 12)

Calculate the nominal interest rate if the periodic interest rate is 2.0875% per quarter. (Answer: 8.35% compounded quarterly)

After a period of three months, Alese saw one interest deposit of $176.40 for a principal of $9,800. What nominal rate of interest is Alese earning? (Answer: 7.21 compounded quarterly)

The simplest future value scenario for compound interest is for all of the variables to remain unchanged throughout the entire transaction. To understand the derivation of the formula, continue with the following scenario. If $4000 was borrowed two years ago at 12% compounded semi-annually, then a borrower will owe two years of compound interest in addition to the original principal of $4,000. That means PV">PV = $4,000. The compounding frequency is semi-annually, or twice per year, which makes the periodic interest rate i=12%2=6%">. Therefore, after the first six months, the borrower has 6% interest converted to principal. This a future value, or FV">FV, calculated as follows:

Principal after one compounding period (six months) = Principal plus interest

Now proceed to the next six months. The future value after two compounding periods (one year) is calculated in the same way.

Note that the equation can be factored and rewritten as .

Since the is the result of the previous calculation where , the following algebraic substitution is possible:

Simplifying algebraically, you get:

Do you notice a pattern? With one compounding period, the formula has only one (1+i)">. With two compounding periods involved, it has two factors of . Each successive compounding period multiplies a further onto the equation. This makes the exponent on the exactly equal to the number of times that interest is converted to principal during the transaction.

The Formula

First, you need to know how many times interest is converted to principal throughout the transaction. You can then calculate the future value. Use Formula 9.2A below to determine the number of compound periods involved in the transaction.

where,

C/Y is the number of compounding periods per year.

Once you know n, substitute it into Formula 9.2B, which finds the amount of principal and interest together at the end of the transaction, or the future (maturity) value, FV.

where,

PV is the resent value or principal. This is the starting amount upon which compound interest is calculated.

i is the periodic interest rate from Formula 9.1.

n is the number of compound periods from Formula 9.2A.

Important Notes

Calculating the Interest Amount (I):

In any situation of lump-sum compound interest, you can isolate the interest amount using the formula

.

How It Works

Follow these steps to calculate the future value of a single payment:

Step 1: Calculate the periodic interest rate (i) using the formula

Step 2: Calculate the total number of compound periods (n) using the formula

Step 3: Calculate the future value using the formula

Note: You will first need to calculate i and n using steps 1 and 2.

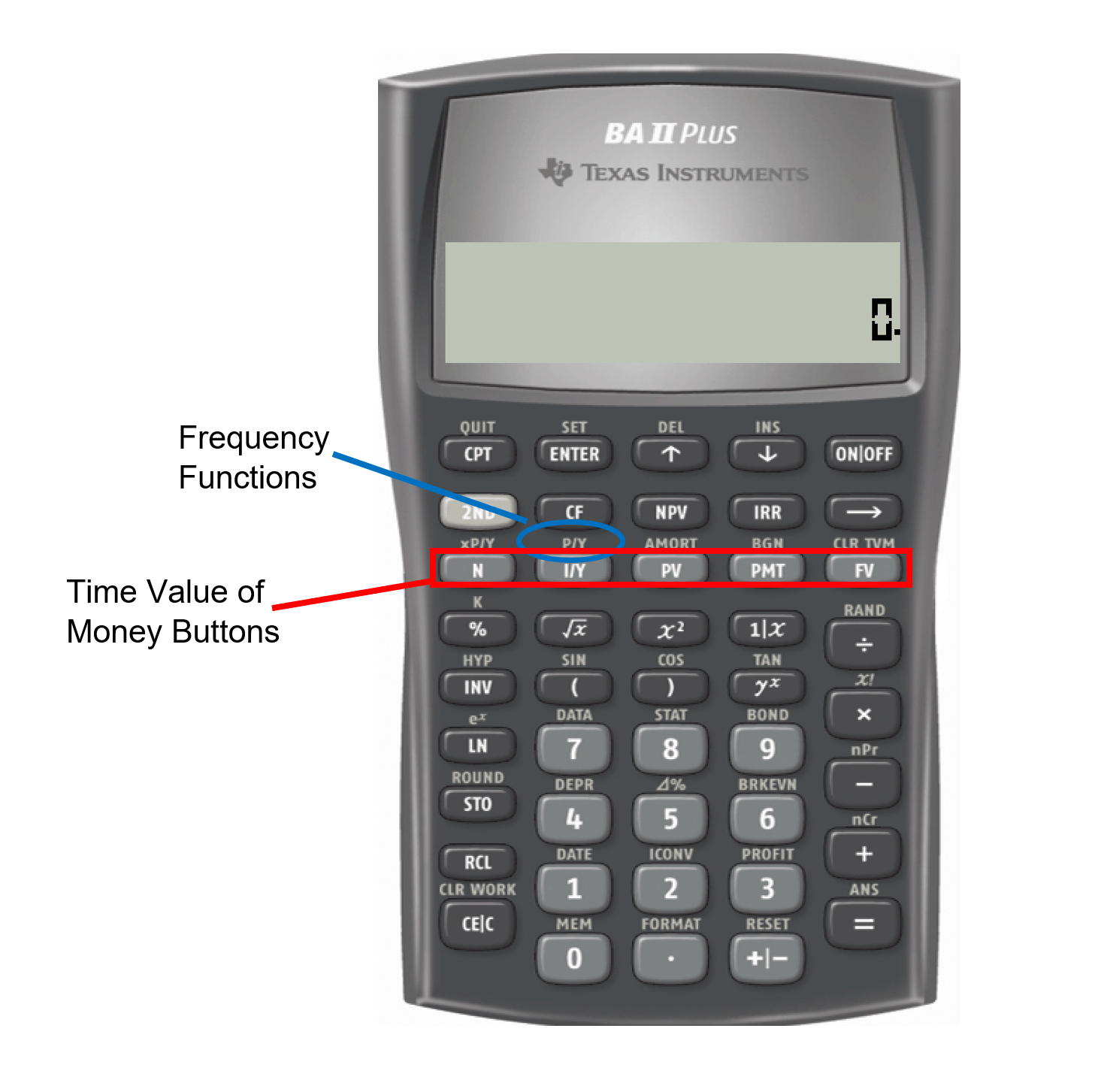

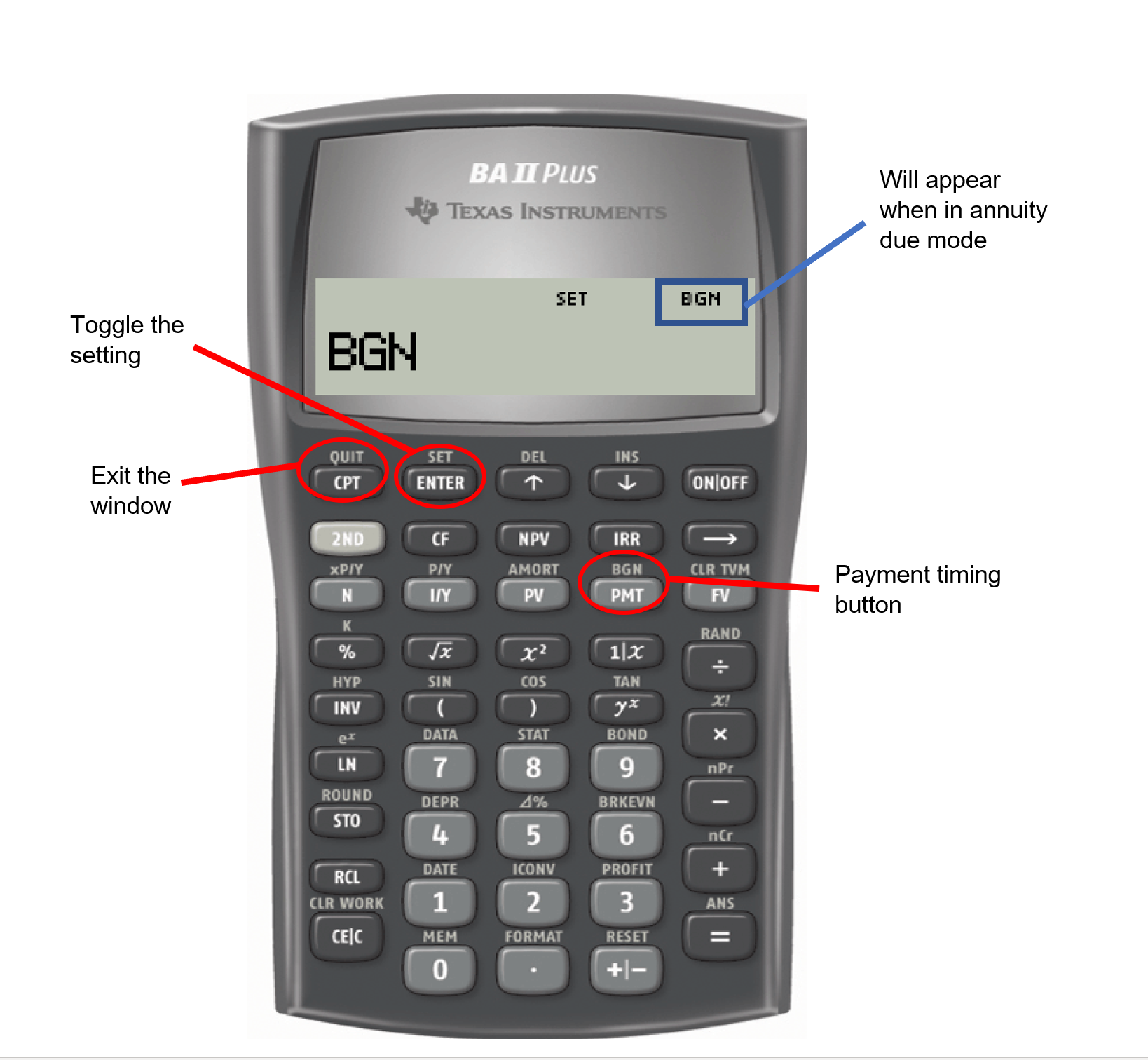

Your BAII Plus Calculator

We will be using the function keys that are presented in the third row of your calculator, known as the TVM row or (time value of money row). The five buttons located on the third row of the calculator are five of the seven variables required for time value of money calculations. This row’s buttons are different in colour from the rest of the buttons on the keypad.

Figure 9.2.0 Texas Instrument BAII Plus Calculator [Image Description]

The table below relates each button (variable) to its meaning.

Table 9.2.1. BA II Plus Calculator Variables and Meanings

Variable

Meaning

N

Number of compounding periods

I/Y

Interest rate per year (nominal interest rate). This is entered in percent form (without the % sign). For example, 5% is entered as 5.

PV

Present value or principal

PMT

Periodic annuity payment. For lump sum payments set this variable to zero.

FV

Future value or maturity value.

C/Y

Pressing 2ND key then I/Y will open the P/Y worksheet. P/Y stands for periodic payments per year and this will be covered in annuities. We only need to assign a value for C/Y as the calculation does not involve an annuity. We need to set payments per year (P/Y) to the same value as the number of compounding periods per year (C/Y) then press ENTER. When you scroll down (using the down arrow key), you will notice that C/Y will automatically be set to the same value. Pressing 2nd then CPT (Quit button) will close the worksheet.

To enter any information into any one of these buttons, key in the data first and then press the appropriate button. For example, if you want to enter N = 34, then key in 34 followed by pressing N.

Cash Flow Sign Convention

Calculating FV (PV is given)

For investments: When money is invested (paid-out), this amount is considered as a cash-outflow and this amount has to be entered as a negative number for PV.

For Loans: When money is received (loaned), this amount is considered as a cash-inflow and this amount has to be entered as a positive number for PV.

Calculating PV (FV is given)

For investments: When you receive your matured investment at the end of the term this is considered as a cash-inflow for you and the future value should be entered as a positive amount.

For Loans: When the loan is repaid at the end of the term this is considered as a cash-outflow for you and the future value should be entered as a negative amount.

Important Notes

When you compute solutions on the BAII Plus calculator, one of the most common error messages displayed is “Error 5.” This error indicates that the cash flow sign convention has been used in a manner that is financially impossible. Some examples of these financial impossibilities include loans with no repayment or investments that never pay out. In these cases, the PV and FV have been incorrectly set to the same cash flow sign.

BAII Plus Memory

Your calculator has permanent memory. Once you enter data into any of the time value buttons it is permanently stored until

You override it by entering another piece of data and pressing the button;

You clear the memory of the time value buttons by pressing 2nd CLR TVM before proceeding with another question; or

The reset button on the back of the calculator is pressed.

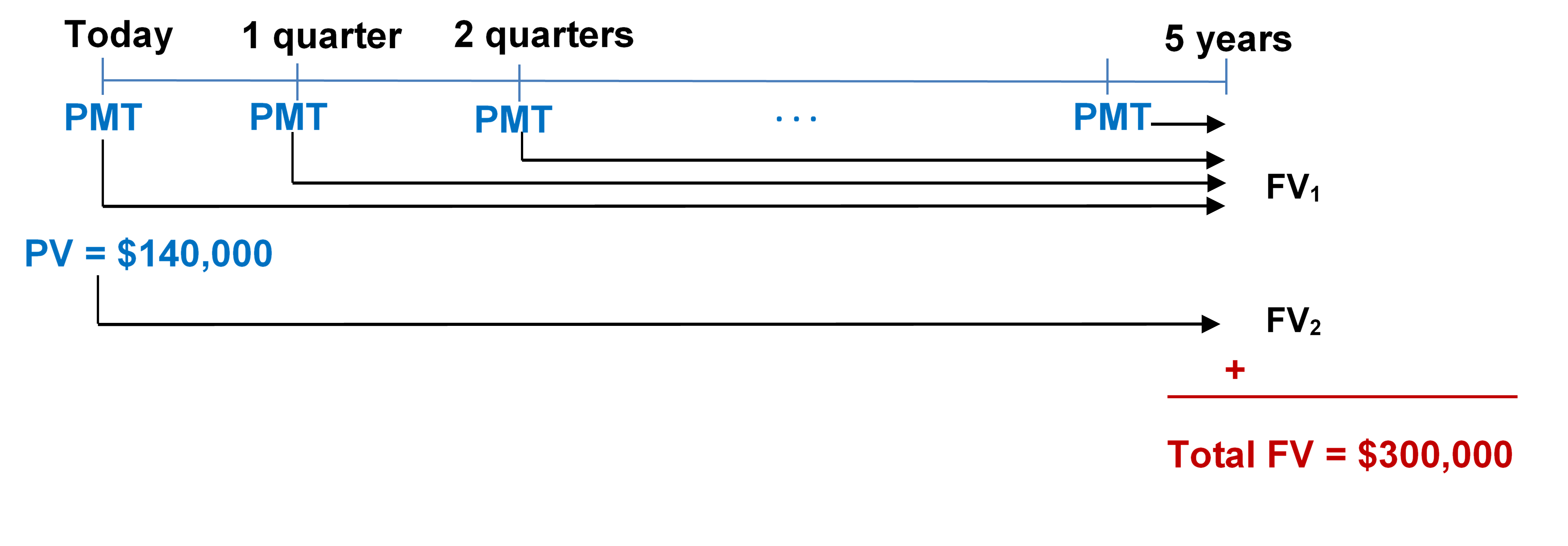

Example 9.2.1: Making an Investment

If you invested $5,000 for 10 years at 9% compounded quarterly, how much money would you have? What is the interest earned during the term?

Step 3: Calculate the total number of compoundings, n.

Step 4:Solve for the future value, FV.

Step 5:Find the interest earned.

Calculator instructions:

Table 9.2.2. Calculator Instructions for Example 9.2.1

N

I/Y

PV

PMT

FV

P/Y

C/Y

40

9

-5,000

0

?

12

12

After 10 years, the principal grows to $12,175.94, which includes your $5,000 principal and $7,175.94 of compound interest.

Future Value Calculations with Variable Changes

What happens if a variable such as the nominal interest rate, compounding frequency, or even the principal changes somewhere in the middle of the transaction? When any variable changes, you must break the timeline into separate time fragments at the point of the change. To arrive at the solution, you need to work from left to right one time segment at a time using the future value formula.

How It Works

Follow these steps when variables change in calculations of future value based on lump-sum compound interest:

Step 1: Read and understand the problem. Identify the present value. Draw a timeline broken into separate time segments at the point of any change. For each time segment, identify any principal changes, the nominal interest rate, the compounding frequency, and the length of the time segment in years.

Step 2: For each time segment, calculate the periodic interest rate (i) using Formula 9.1.

Step 3: For each time segment, calculate the total number of compound periods (n) using Formula 9.2A.

Step 4: Starting with the present value in the first time segment (starting on the left), solve for the future value using Formula 9.2B.

Step 5: Let the future value calculated in the previous step become the present value for the next step. If the principal changes, adjust the new present value accordingly.

Step 6: Using Formula 9.2B calculate the future value of the next time segment.

Step 7: Repeat steps 5 and 6 until you obtain the final future value from the final time segment.

Important Notes

The BAII Plus Calculator:

Transforming the future value from one time segment into the present value of the next time segment does not require re-entering the computed value. Instead, apply the following technique:

Load the calculator with all known compound interest variables for the first time segment.

Compute the future value at the end of the segment.

With the answer still on your display, adjust the principal if needed, change the cash flow sign by pressing the ± key, and then store the unrounded number back into the present value button by pressing PV. Change the N, I/Y, and C/Y as required for the next segment.

Return to step 2 for each time segment until you have completed all time segments.

Five years ago Coast Appliances was supposed to upgrade one of its facilities at a quoted cost of $48,000. The upgrade was not completed, so Coast Appliances delayed the purchase until now. The construction company that provided the quote indicates that prices rose 6% compounded quarterly for the first 1½ years, 7% compounded semi-annually for the following 2½ years, and 7.5% compounded monthly for the final year. If Coast Appliances wants to perform the upgrade today, what amount of money does it need?

Solution:

The timeline below shows the original quote from five years ago until today.

Table 9.2.3. Calculator Instructions for Steps 1-3, Example 9.2.2.

Step

N

I/Y

PV

PMT

FV

P/Y

C/Y

1

6

6

48,500

0

?

4

4

2

5

7

52,485.27667

0

?

2

2

3

12

7.5

62,336.04435

0

?

12

12

Coast Appliances requires $67,175.35 to perform the upgrade today. This consists of $48,000 from the original quote plus $19,175.35 in price increases.

Example 9.2.3: Making an Additional Contribution

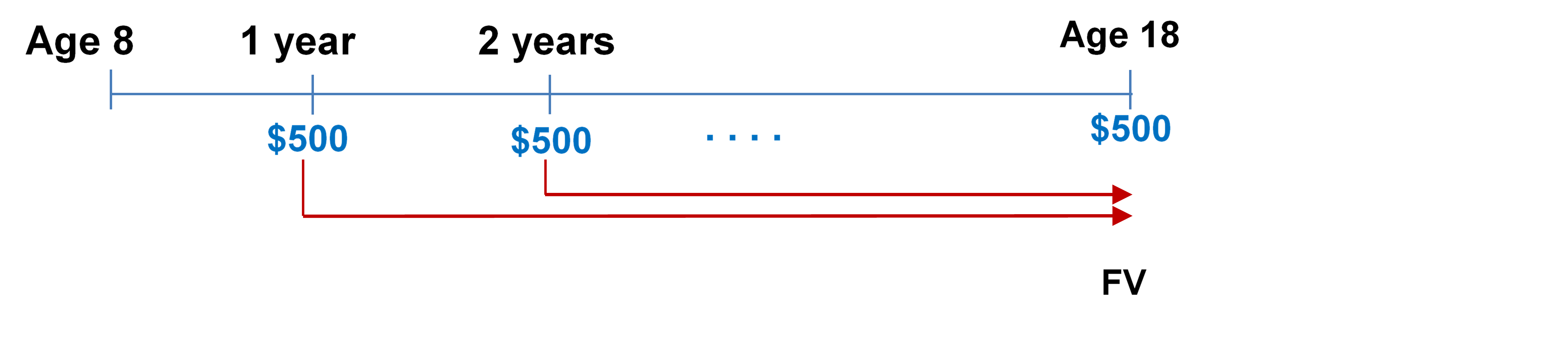

Two years ago Lorelei placed $2,000 into an investment earning 6% compounded monthly. Today she makes a deposit to the investment in the amount of $1,500. What is the maturity value of her investment three years from now?

Table 9.2.4. Calculator Instructions for Example 9.2.3

Step

N

I/Y

PV

PMT

FV

P/Y

C/Y

1

24

6

-2,000

0

?

12

12

2

36

6

-3,754.319552

0

?

12

12

Three years from now Lorelei will have $4,492.72. This represents $3,500 of principal and $992.72 of compound interest.

Exercises

In each of the exercises that follow, try them on your own. Full solutions are available should you get stuck.

Find the future value if $53,000 is invested at 6% compounded monthly for 4 years and 3 months.(Answer: $68,351.02)

Find the future value if $24,500 is invested at 4.1% compounded annually for 4 years; then 5.15% compounded quarterly for 1 year, 9 months; then 5.35% compounded monthly for 1 year, 3 months. (Answer: $33,638.67)

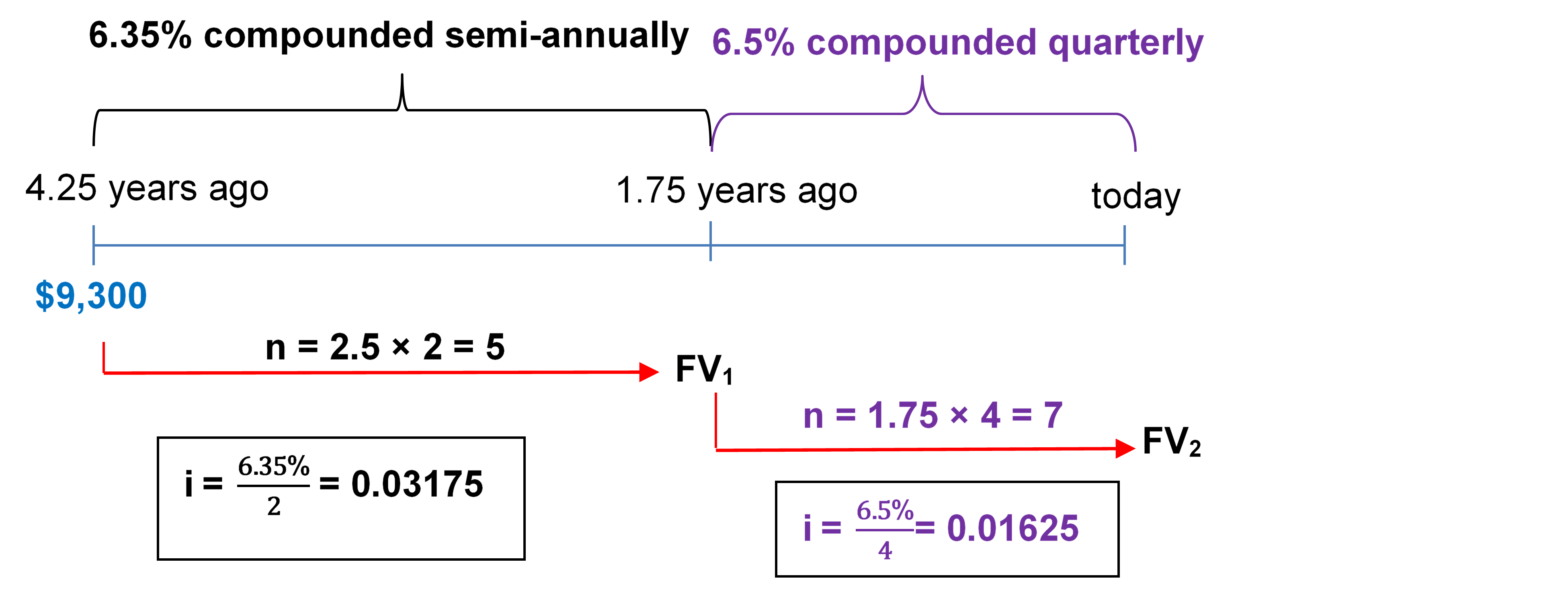

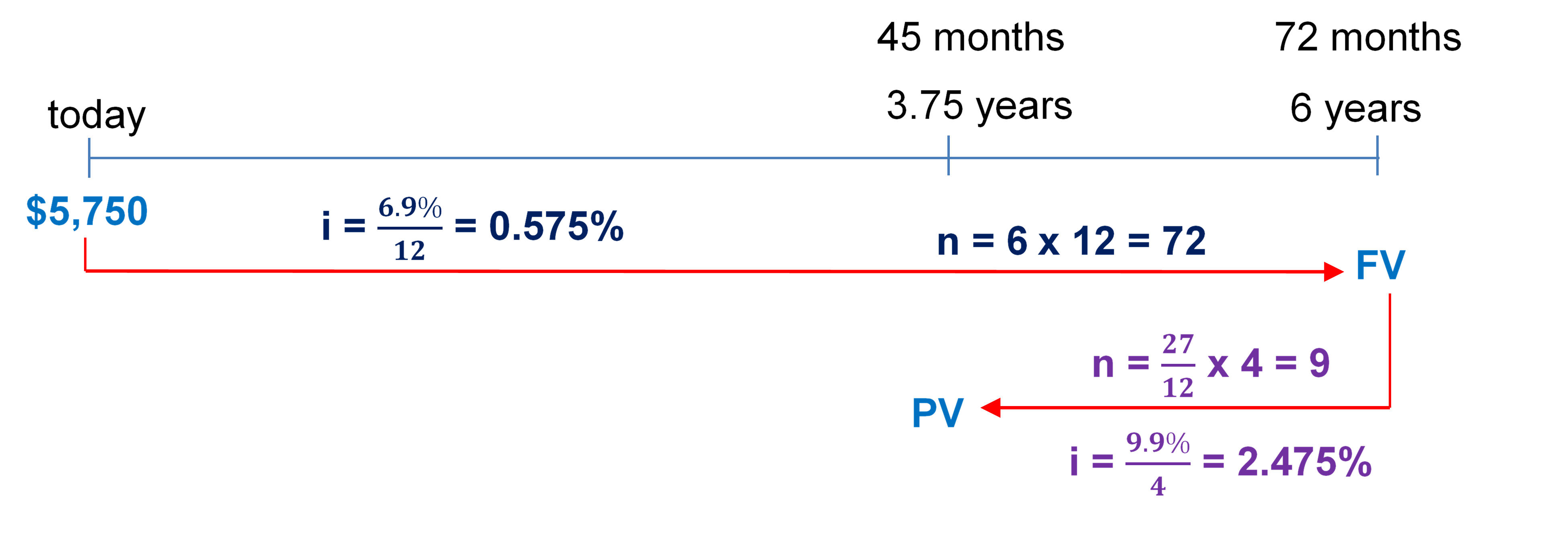

Nirdosh borrowed $9,300 4¼ years ago at 6.35% compounded semi-annually. The interest rate changed to 6.5% compounded quarterly 1¾ years ago. What amount of money today is required to pay off this loan?(Answer: $12,171.92)

Figure 9.2.0: Picture of the BAII Plus calculator showing the “Frequency Functions”, and the “Time Value of Money Buttons”.[Back to Figure 9.2.0]

Figure 9.2.1: Timeline showing PV =$35,000 at Today (on the Left) with an arrow pointing to the end (on the Right) (10 years) where FV = ? and 9% quarterly throughout. [Back to Figure 9.2.1]

Figure 9.2.2: Timeline: PV1 = $48,000 at 5 years ago moving to 3.5 years ago at 6% quarterly to become FV1. At 3.5 years ago, FV1 becomes PV2 which moves to 1 year ago at 7% semi-annually to become FV2. At 1 years ago, FV2 becomes PV3 which moves to Today at 7.5% monthly to become FV3 = ?. [Back to Figure 9.2.2]

Figure 9.2.3: Timeline: At 2 years ago, FV1 = $2,000 moves to Today at 6% monthly to become FV1. At Today, there is a$1,500 deposit. At Today, FV1 becomes PV2 which moves to 3 years at 6% monthly to become FV2 = ?. [Back to Figure 9.2.3]

9.3: Determining the Present Value

12

Determining the Present Value

PV is the Present Value or Principal. This is the new unknown variable. If this is in fact the amount at the start of the financial transaction, it is also called the principal. Or it can simply be the amount at some earlier point in time than when the future value is known. In any case, the amount excludes the future interest. To calculate this variable, substitute the values for the other three variables into the formula and then algebraically rearrange to isolate PV.

The Formula

Solving for present value requires you to use the future value formula we introduced in section 9.2 (Formula 9.2B). We rearrange the future value formula to solve for P.

How It Works

Follow these steps to calculate the present value of a single payment:

Step 1: Calculate the periodic interest rate (i) using the formula

Step 2: Calculate the total number of compound periods (n) usingtheformula

Step 3: Calculate the present value using the present value formula

Your BAII Plus Calculator

You use the financial calculator in the exact same manner as described in Section 9.2. The only difference is that the unknown variable is PV instead of FV. You must still load the other six variables into the calculator and apply the cash flow sign convention carefully.

Example 9.3.1: Achieving a Savings Goal

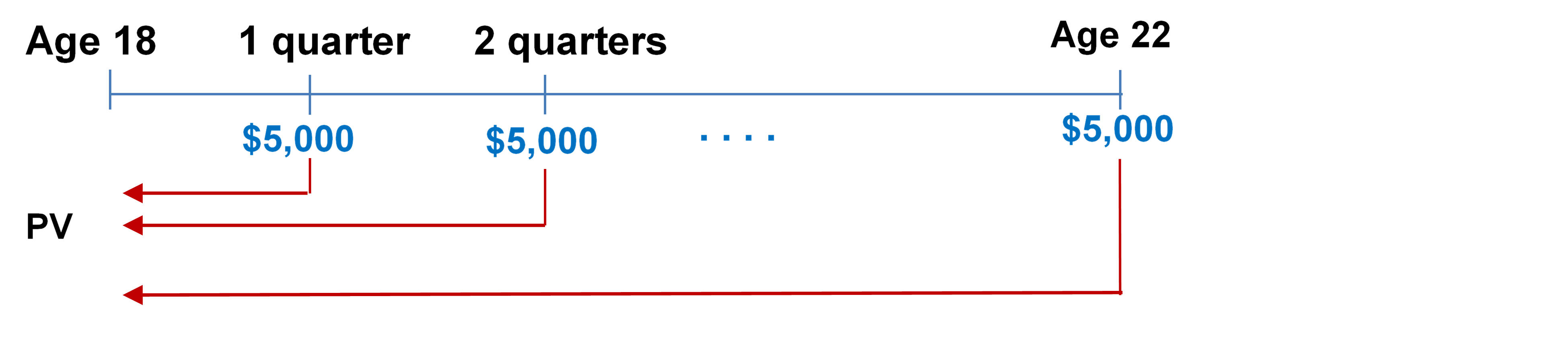

Castillo’s Warehouse will need to purchase a new forklift for its warehouse operations three years from now, when its new warehouse facility becomes operational. If the price of the new forklift is $38,000 and Castillo’s can invest its money at 7.25% compounded monthly, how much money should it put aside today to achieve its goal?

Step 3: Calculate the number of compound periods, n.

Step 4: Solve for the present value, PV.

Table 9.3.1. Calculator Instructions for Example 9.3.1

N

I/Y

PV

PMT

FV

P/Y

C/Y

36

7.25

?

0

38,000

12

12

If Castillo’s Warehouse places $30,592.06 into the investment, it will earn enough interest to grow to $38,000 three years from now to purchase the forklift.

Present Value Calculations with Variable Changes

Addressing variable changes in present value calculations follows the same techniques as future value calculations. You must break the timeline into separate time segments, each of which involves its own calculations.

Solving for the unknown PV at the left of the timeline means you must start at the right of the timeline. You must work from right to left, one time segment at a time using the formula for PV each time. Note that the present value for one time segment becomes the future value for the next time segment to the left.

How It Works

Follow these steps to calculate a present value involving variable changes in single payment compound interest:

Step 1: Read and understand the problem. Identify the future value. Draw a timeline broken into separate time segments at the point of any change. For each time segment, identify any principal changes, the nominal interest rate, the compounding frequency, and the segment’s length in years.

Step 2: For each time segment, calculate the periodic interest rate, i.

Step 3: For each time segment, calculate the total number of compounding periods, n.

Step 4: Starting with the future value in the first time segment on the right, solve for the present value.

Step 5: Let the present value calculated in the previous step become the future value for the next time segment to the left. If the principal changes, adjust the new future value accordingly.

Step 6: Using the present value formula, calculate the present value of the next time segment.

Step 7: Repeat steps 5 and 6 until you obtain the present value from the leftmost time segment.

Your BAII Plus Calculator

To use your calculator efficiently in working through multiple time segments, follow a procedure similar to that for future value:

Load the calculator with all the known compound interest variables for the first time segment on the right.

Compute the present value at the beginning of the segment.

With the answer still on your display, adjust the principal if needed, change the cash flow sign by pressing the key, then store the unrounded number back into the future value button by pressing FV. Change the N, I/Y, and C/Y as required for the next segment.

Return to Step 2 for each time segment until you have completed all time segments.

Example 9.3.2: A Variable Rate Investment

Sebastien needs to have $9,200 saved up three years from now. The investment he is considering pays 7% compounded semi-annually, 8% compounded quarterly, and 9% compounded monthly in successive years. To achieve his goal, how much money does he need to place into the investment today?

Table 9.3.2. Calculator Instructions for Example 9.3.2

Step

N

I/Y

PV

PMT

FV

P/Y

C/Y

1

12

9

?

0

9,200

12

12

2

4

8

?

0

±(PV from Step 1)

4

4

3

2

7

?

0

±(PV from Step 1)

2

2

Sebastien needs to place $7,253.80 into the investment today to have $9,200 three years from now.

When you calculate the present value of a single payment for which only the interest rate fluctuates, it is possible to find the principal amount in a single division:

where represents the time segment number.

In the previous example you can calculate the same principal as follows:

Exercises

In each of the exercises that follow, try them on your own. Full solutions are available should you get stuck.

A debt of $37,000 is owed 21 months from today. If prevailing interest rates are 6.55% compounded quarterly, what amount should the creditor be willing to accept today? (Answer: $33,023.56)

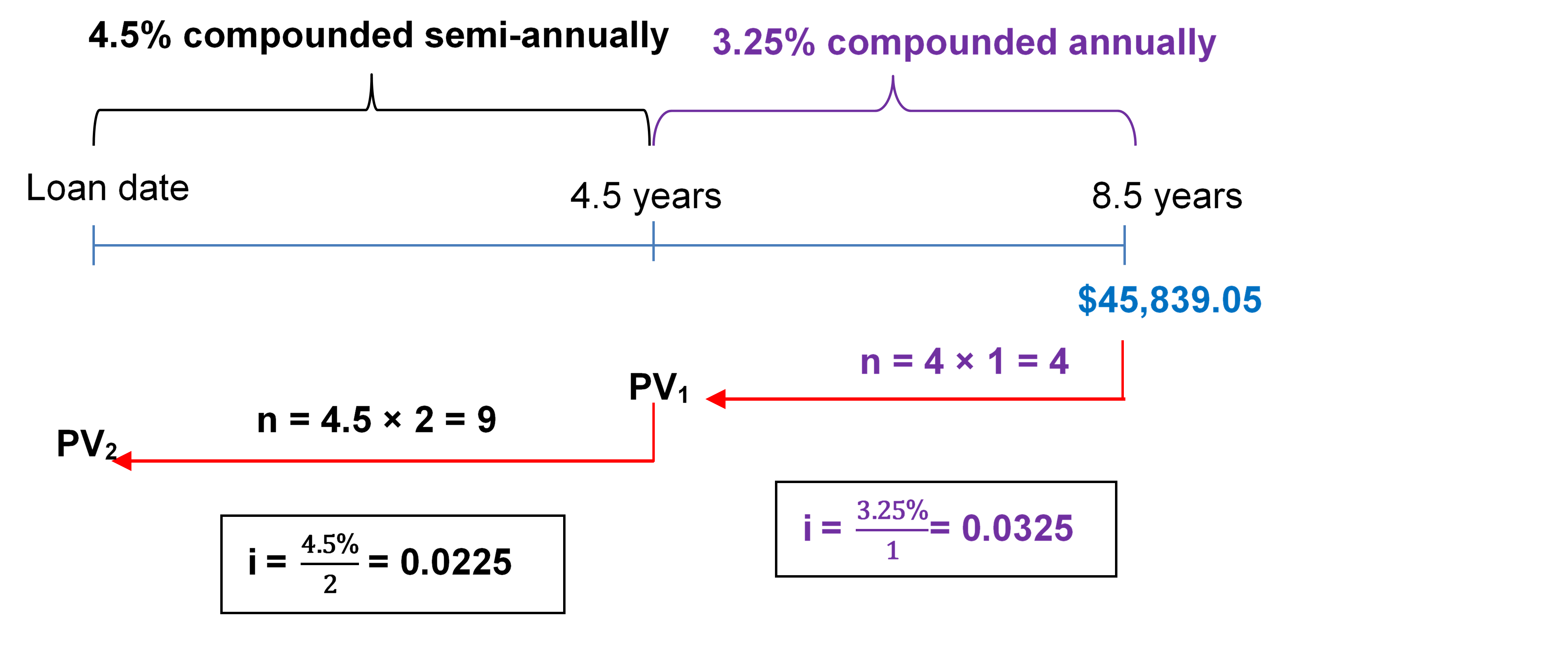

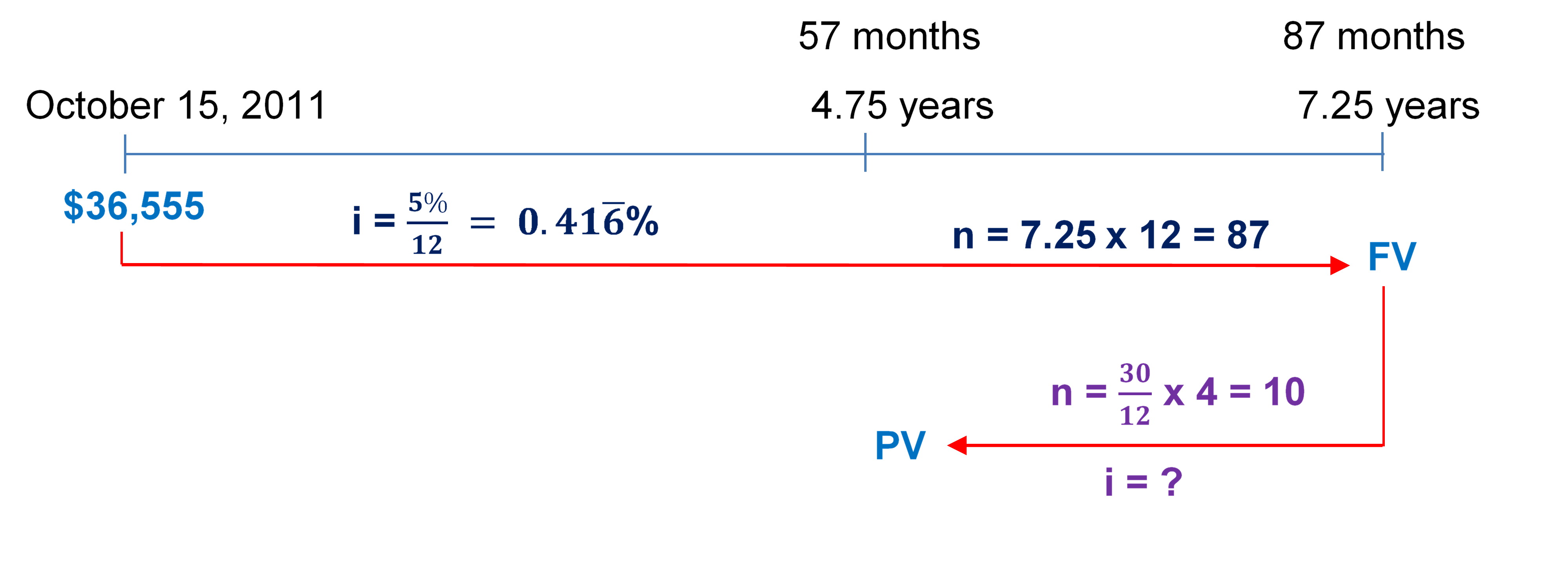

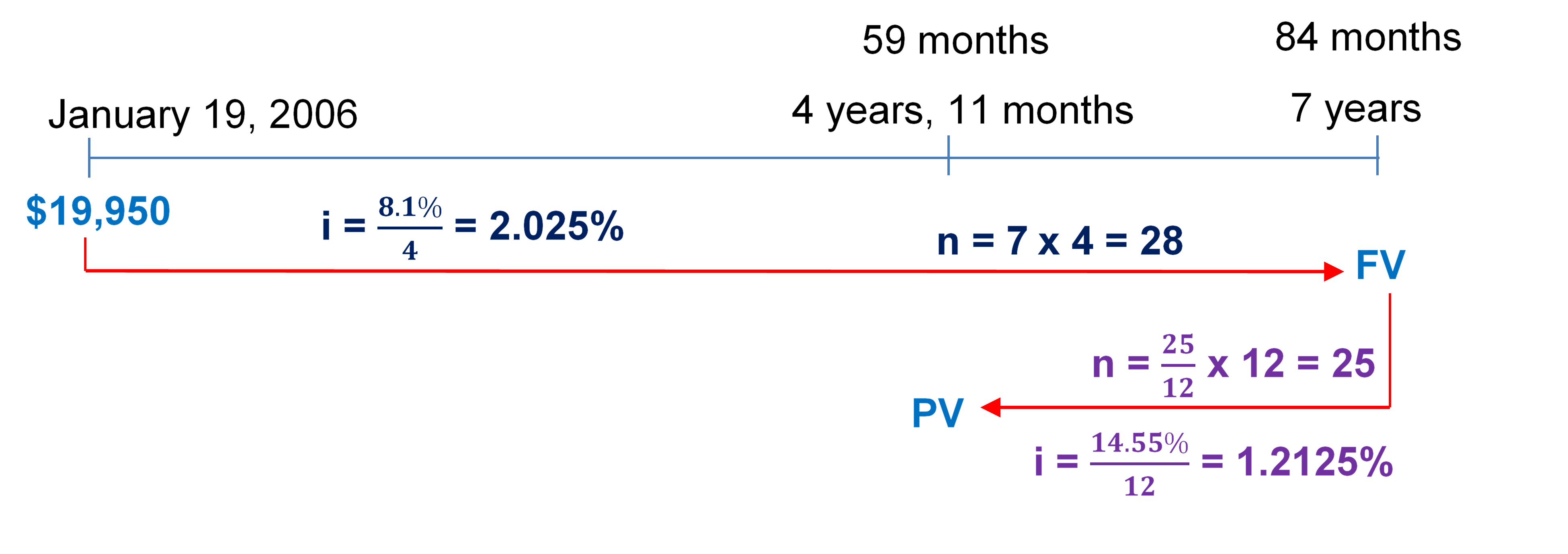

For the first 4½ years, a loan was charged interest at 4.5% compounded semi-annually. For the next 4 years, the rate was 3.25% compounded annually. If the maturity value was $45,839.05 at the end of the 8½ years, what was the principal of the loan?(Answer: $33,014.56)

Figure 9.3.1: Timeline showing PV = ? at Today (on the Left) with an arrow pointing to the end (on the Right) (3 years) where FV = $38,000 and 7.25% monthly throughout. [Back to Figure 9.3.1]